By Tom Luongo

March 23, 2023

So, Credit Suisse is no more. Good riddance? I think this is an open question given the very complicated landscape of the global banking system today. By the time I'm done here I think you'll have an answer that no one, including me, was expecting.

There's a lot to cover, so let's start at the beginning.

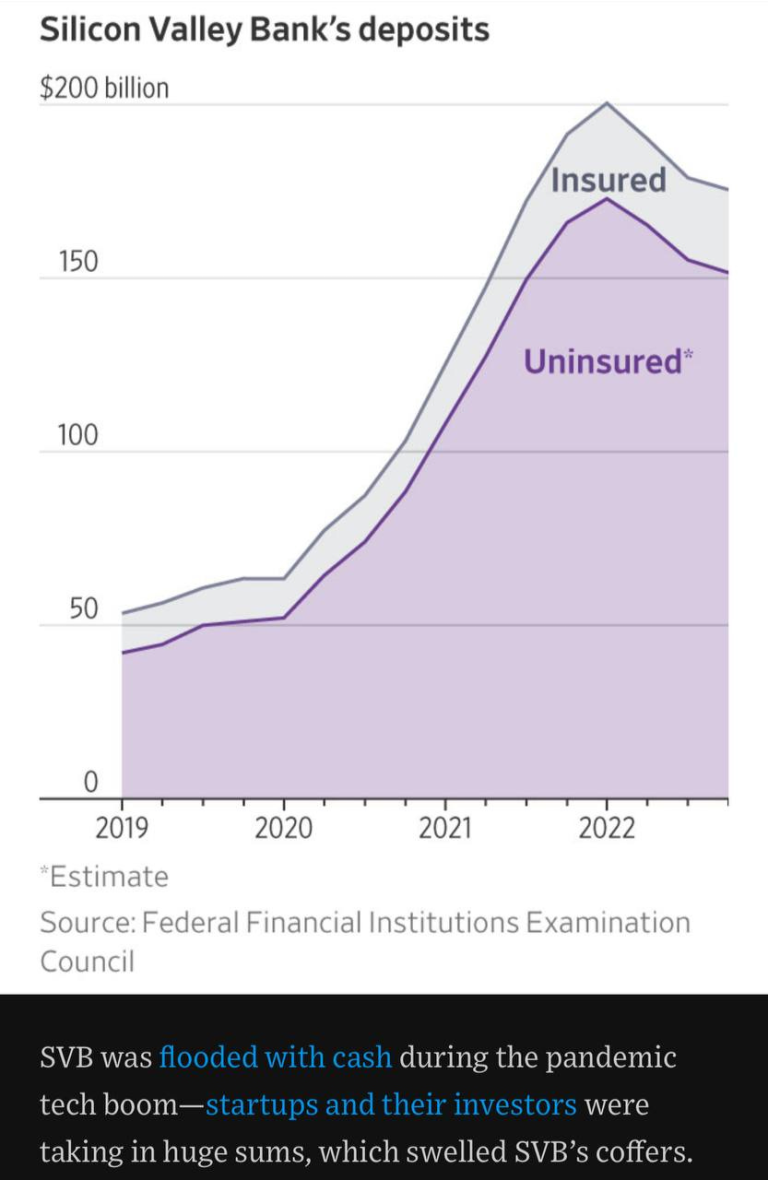

In the wake of the "three-fer" take out of Silvergate, Silicon Valley and Signature banks by the 'market' I think we have a pretty clear picture of what's really going on.

This wasn't a 'market' operation. It was a Fed/NY Boys operation and a very successful one.

The Fed (and only the Fed through its proxies) had the motive, means and opportunity to perform the hit job. I wrote a big post for my patrons on March 11th (now made public) going over this.

These Three S's were all operating as offshore Shadow banks. As Phil Gibson pointed out on his most recent Substack article:

SVB ultimately runs its funding the way Startup funding does:

- A person with $1b comes in and puts $1b into SVB. They go out to a startup and sign a term sheet. This sheet says that the startup will deposit its money in SVB.

- Then SVB goes out and loans that $1b out to another VC. Who 'invests' it in another startup, who's term sheet says they will keep their deposits in SVB.

- So now SVB has take $1b dollars and made it $2b dollars. Without any fed regulation or intervention.

To which I would add the deposits coming back in were then invested in long-dated US Treasuries and marked as 'hold to maturity.' This meant they couldn't be sold. This was a good deal as long as the short-end of the yield curve stayed at the zero-bound, or at least below that of the long-end.

As the Fed raised rates, well, not so much. Too bad, so sad, see you at the Auto Show, SVB.

Rates rising were one thing impairing SVB's balance sheet but the inversion of the US yield curve didn't help things either. All it took was a whisper campaign by people with three working brain cells to see the situation for what it was and execute the bank.

Easy peesy, bank run squeezy.

A lot of people have been all over the Fed for this screaming that the Big Banks are rolling up the small banks, but if that were the case why have no other small banks failed?

Why did the Bank Term Funding Program (BTFP) basically allow the Regional banks who had similar holes in their balance sheets to SVB (but who also had risk management officers on staff!) to swap them at par with the Fed at a fixed-term rather than forcing them onto the Walk of Shame to the Discount Window?

Bueller? Frye?

It's because the BTFP actually saved the regional banks, while simultaneously raising FDIC insurance for insured accounts to infinity and beyond. And while that is a real problem of moral hazard which the Fed and the US will pay for later, it was absolutely the right strategic move from the Fed's perspective today.

It also created a virtuous cycle for the onshoring of US Treasuries now that the US banking system will need high quality collateral to offset higher savings rates that are inevitable thanks to the Fed taking the smaller banks under its protection.

The ones screaming for the Fed to lower rates and go back to QE are the ones who can't use the BTFP or they are gold bugs who need to be right that this is it, this is the day they get vindicated for years of being myopic putzes thinking only gold is the answer.

Don't even get me started on the Bitcoin Maxis.

When, honestly, tboth groups refuse to realize they are simping for the very people who have ensured that gold and bitcoin stay on the margins of the financial system through egregious leverage for more than a decade.

But, I digress.

In effect, the swiftness with which the Fed acted (and crammed an unpalatable solution down Janet Yellen's throat) actually shores up the regional banks while leaving the Fed free now to continue raising rates and shrinking its balance sheet all while increasing the demand for US Treasuries during a period of intense de-dollarization.

The price? A few extra billions of rent was paid off to the thieves. But, that's it. The spigot has been closed, the stopcock broken off and the valve filled with molten lead. Gone. Done.

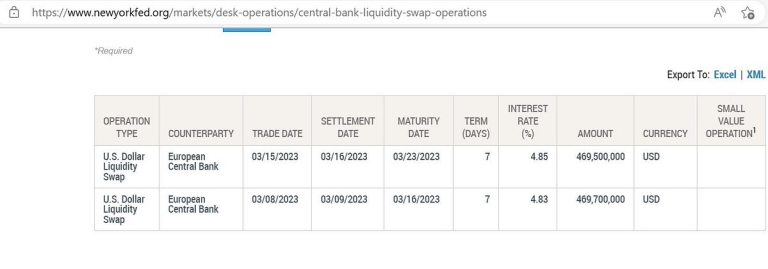

Well, except a few here and there via swap lines to make it look like they aren't heartless.

But please note the ECB got the same terms on a USD/Euro swap that the Regional Banks get from the Fed. We didn't see Powell announce an emergency rate cut or anything like that.

If anyone did the bank Walk of Shame it was the ECB.

The point of my opening argument is that the Fed did exactly what it was chartered to do here.... protect the US banking system. And it did that while paying lip service to coordinating central bank policy to keep US dollar funding markets liquid, which is also part of its job, as long as it is in service of its primary job, protecting US banks.

And, as I've argued over and over, while there are still massive holes in the global financial system because there aren't enough dollars to go around, the Fed is now in control of who gets those dollars. Watching who does and who doesn't get preferential treatment is now the key to understanding what happens next.

You, Me and the FDIC

Right up until his death, the Calvinist OG of the Austrian Economic Sewing Circle, Dr. Gary North, wrote about FDIC and its importance in ending the Great Depression. He wrote volumes on the subject. North understood better than nearly everyone that fractional reserve banking is a confidence game.

And FDIC in the US is the bedrock on which confidence in the post-Great Depression US Empire was built. Well, okay, FDIC, the Marshall Plan, LIBOR, and the whole Eurodollar global reserve fantasy world if you want to be pedantic.

Whether you agree with fractional reserve banking or not is irrelevant. It exists, is the paradigm on which our banking system operates, and has very predictable fault lines within it guaranteeing bank runs at some point.

Milton Friedman and his disciples are wrong about what started and stopped the Great Depression. Capital flight out of Europe because of a sovereign debt crisis sent US equity markets to new highs thanks to a strong US dollar, per Martin Armstrong's analysis, and North was right that FDIC was the only thing that curbed the demand to hoard dollars under mattresses and put them back to work in the banking system.

So, read his 2019 missive explaining the situation in the aftermath of the Repo Crisis and think through the massive liquidity injection by Keynesians in our government in "response" to COVID-19, which FOMC Chair Jerome Powell argued against, and you'll see echoes of where we are today.

Under today's circumstances {2019}, the money supply will not shrink. The money supply is based on how much debt the Federal Reserve System has in its reserves: the monetary base. {In 2023, the Fed is shrinking its reserves} The fact that depositor A in busted Bank A has lost his money does not shrink the money supply. Another depositor, who was paid by borrower B (e.g., a mortgage borrower) at Bank A, still has his deposit in Bank B. The banking system does not lose money. But doubts spread about the economy. People start moving their portfolios toward near-cash assets. They start selling stocks so that they can buy Treasury bills or T-bonds.

To North's point about selling stocks to buy US Treasuries, today is different because there is a massive stock of money in the Reverse Repo Facility but the dynamic is the same. As the Fed raises rates money is flowing out of where it is into Money Markets and variable rate US Treasuries, as Ted Oakley suggested in my last podcast with him.

People are getting to near-cash assets as the Fed raised rates.

This has been going on all year {2019}. The 90-day T-bill rate is under 2%. It fell before the Federal Reserve announced its reduction in the federal funds overnight market. The FED has trailed T-bill rate all year. The FED gets credit for lowering rates, but this has been an illusion in 2008. The FED has been playing catch-up with the T-bill rate. It announces what T-bills have already achieved: lower rates.

The Fed did the opposite of what the market told it to do in 2019. Powell raised rates fast. He did this to "break something" as Danielle Dimartino Booth said all through 2022.

This is why the "Pivot" crowd is crowing today that the Fed is headed back to the zero-bound and will restart QE. But they are wrong.

I read everything North wrote during the bailouts and advent of QE during the 2008 Financial Crisis as part of my real education. I know he would be part of the pivot crowd because he had no faith in the Fed. And rightly so. None of us did in 2019 and should be skeptical of it in 2023.

But North also understood incentives. He understood that if the Fed broke something the first thing it would do is lobby for raising FDIC limits.

He argued then, rightly so, that FDIC expansion was the right step then and eventually it would go to infinity. Fine, no argument there. Nothing is off the table when the Fed is out to protect the US banks.

And right on schedule, when a few particular regional banks of dubious character (and allegiance) blew up, Powell gets Yellen to agree to unlimited FDIC insurance for insured accounts (not, crucially important here, uninsured accounts) while also filling the holes on the Regional Banks' balance sheets.

This was the main thing Powell did to put the US banking system in a superior position to all the other banking systems. We have the ability to absorb these depositor losses and the political incentives line up to ensure that occurs, from both sides of the populist political aisles.

Even Elizabeth Warren can't complain about what the Fed did here.

But North also was right about Bernanke's sterilization of QE through another Fed manipulation of capital flow, Interest on Excess Reserves (IOER). He argued, rightly in 2009, that IOER would be stagflationary, creating the financialized world we have today but where the real economy would suffer from constraints having to compete for capital with any idiotic idea out there because money was free.

The slow growth era of the Coordinated Central Bank Policy Era was instrumental in hollowing out what was left of Main Street.

Et Voila, 2023.

And that brings me, finally, to Credit Suisse.

Burning Down the Haus

One of my favorite heuristics in analyzing big moments in history is to look at who is saying nothing and who is bitching.

Whoever is bitching is vulnerable and getting the shaft, especially if they are aligned with certain groups of people, in this case the devil we all know, The Davos Crowd.

Whoever is saying nothing is winning. Notice that Jamie Dimon isn't saying anything other than helping to shore up First Republic Bank with JPM's own capital? As Luke Gromen would say, "Signpost!"

So, here's your timeline of events leading up to this weekend.

- The US/EU force Russia's hand into invading Ukraine in Feb. 2022

- The US/EU try to destroy Russia setting off a liquidity spiral of insane commodity prices

- The Fed raises rates to combat inflation while having decoupled US banks mostly from Europe

- SOFR overtakes the Eurodollar as the US dollar funding vehicle of choice.

- The Swiss gov't gives up their centuries old neutrality by backing Ukraine publicly

- The Swiss President is clearly a compromised figure, undermining Swiss sovereignty for the Great Reset (See my Podcasts with Pascal Najadi on this. Episodes #122 and # 132)

- Because of this Switzerland starts seeing capital outflow b/c it's no longer neutral

- During the takeover of the UK last summer, Credit Suisse comes under attack, forcing the Fed to shore it up through swap lines to the SNB.

- The Fed keeps raising rates forcing the ECB to follow.

- Eurodollar liquidity collapses, the BoJ begins giving up Yield Curve Control.

- Russia keeps grinding out the Ukrainian Army in the Donbass

- Once the Fed breaks the Three S's Davos counters by 𝕏 pulling their liquidity from CS.

- The run on CS intensifies forcing the SNB and UBS into action.

- They screw the AT1/CoCo bondholders.

The question raised by #14 is why? Why not let them get their shekels?

This is a clear assault on the vestiges of Swiss sovereignty and the credibility of its banking system, on which the entire country's reputation is based. To think that they wouldn't bend the rules on who gets paid first in this situation is hopelessly naïve.

So, this morning everyone in Europe is furious over the forced merger of UBS and Credit Suisse. For the record I put out what I thought strategically about Credit Suisse and why it would never be allowed to go under:

Famously, the SNB holds a big equity portfolio, at last count ~$139B. These are mostly US large caps. /1

SWISS NATIONAL BANK Top 13F HoldingsDetailed Profile of SWISS NATIONAL BANK portfolio of holdings. SEC Filings include 13F quarterly reports, 13D/G events and more.

The main sticking point for UBS's buyout of Credit Suisse is the 100% write-down of the $17B in "Contingently Convertible" (CoCo) or AT1 bonds, while shareholders of Credit Suisse were put in front of them, getting a few pennies for their previous investments.

Here's the thing. Everyone was wiped out in the Credit Suisse debacle. I believe the point of the attack was to limit the Swiss National Bank's ability to conduct monetary policy by impairing its $139 billion equity portfolio as a way to raise cash and/or supply US stocks to European investors seeking a safe haven from any fallout in Europe.

Moreover, these AT1 or CoCo bonds are effectively permanent bonds, paying out in perpetuity as long as the issuing bank stays solvent. If you take out the bank then they get converted to equity. Knowing that CS was too important to be allowed to fail, I'm betting someone was expecting to force the terms of the bailout.

And the Swiss just said, "Um. No. Sue us."

Oh but you can't because there were covenants in both UBS and Credit Suisse AT1 bonds which allowed for shareholders to be put in front of bondholders. Again from Zerohedge:

As Bloomberg notes, the clauses that led to the bonds being marked to zero aren't common. Only the AT1 bonds of Credit Suisse and UBS Group AG have language in their terms that allows for a permanent write-down and most other banks in Europe and the UK have more protections, according to Jeroen Julius, a credit analyst at Bloomberg Intelligence.

Now, where have I heard about perpetual bonds before? Oh right, from George Soros who wants Europe to default on all of its sovereign debt, wipe out investors, and hand them perpetual bonds as compensation.

Let's put this all together.

UBS bought CS for $3.2 billion. There were $17 billion in Credit Suisse CoCos. As of last Friday's close UBS's market cap was $56.5 billion. That would have made the CoCo holders the biggest ownership group in UBS.

And yet, no one is talking about this.

Does anyone really think UBS would buy Credit Suisse and hand over ownership of their bank at the same time? No. There would be no deal if that were the case.

And what did the UBS term sheet for merging with CS do? Not only did it block the effective takeover of Credit Suisse by the CoCo bondholders who likely were behind the attacks on it in the first place, it impaired the idea of CoCo or perpetual bonds in the minds of investors ensuring that this form of hostile takeover doesn't happen in the future.

This was the only outcome where both the SNB and the Fed maintained any semblance of control over Swiss monetary policy. Merge UBS with Credit Suisse and write the CoCo bonds to zero, freezing out a hostile takeover attempt.

If I don't hear about George Soros having a heart attack in the next 24 hours I will be honestly shocked, because this was clearly something he would have tried to orchestrate.

Here's the money shot folks from Zerohedge (finally getting something right in all of this):

Junior creditors should bear losses only after equity holders have been fully wiped out, according to a joint statement from the Single Resolution Board, the European Banking Authority and the ECB Banking Supervision, who apparently were not consulted on Sunday during the whirlwind decisions that preserved some equity value at CS while wiping out its entire AT1 tranche.

Now why do you think the ECB and European banking authorities weren't consulted on this?

Because this is the key to destroying the capital structure of what's left of the European banks while also hamstringing the SNB.

These AT1 bonds, all $275 billion of them across Europe (okay $258 billion now), were the financial time bombs meant to go off and wipe out the current owners of these banks and transfer them to those who would consolidate power in Europe.

Now, bring back in FDIC. The US has one monolithic FDIC system. Europe doesn't. There are $100,000 insurance programs in individual countries, but no EU program to protect savers. So, think this through. When the banking crisis evolves in Europe the countries will be bailing out their depositors blowing gaping holes in their budgets, which EU rules for many of them will preclude, especially if they are running deficits.

The AT1 bondholders will be gaining control over their banks. The people will be thrown out into the streets.

Depositors over $100,000 will be wiped out. The same fears of small businesses being frozen out of their accounts to make payroll that forced Yellen's hand to go big on FDIC for deposits will play out across Europe.

The entire European commercial banking system will cease to function. It leaves the door open for a massive EU led bailout during the height of the crisis to do what Soros has been demanding they do:

- Have the ECB buy all the outstanding Eurozone debt Convert it all to perpetual bonds, in effect issue new CoCo bonds for the entire Eurozone.

- This is a default on all the sovereign debt and wipes the slate clean This is a default on all the sovereign debt and wipes the slate clean

- Then convert all existing euros to digital euros overnight

- Minority Report with more Germans.

And the people who created the problem will be the ones who implement it because well, they now own all the banks.

But, here's the rub. It is why Europe is furious this morning despite anything that comes out of Christine Lagarde's pie hole, sorry broccoli hole.

The CoCo bond market is now frozen, the bonds are getting gutted. These are some of the most important bits of Tier I capital under Basel III for European banks. Ooops!

Goldman is saying there is now risk of "permanent destruction to demand for AT1 bonds." You don't say Goldman?

The entire idea of CoCo bonds has been undermined by the Swiss and, I think, by extension, the Fed.

On two major fronts, limited insurance for bank deposits and terminally impaired capital structures for European banks, the Fed just positioned the US to be the recipient of major capital inflows as all of the interest rate and credit risk is transferred back to Europe.

This morning I consulted with Dr. North's Ghost:

Tom: What stopped the Great Depression for Real?

Ghost: FDIC

Tom: Why doesn't the EU have this?

Ghost: They thought they owned the Fed

Tom: But they don't.

Ghost: They better hope the Fed still likes them.

Tom: They don't

Ghost: Kek.

Reprinted with permission from Gold Goats 'n Guns.