David Stockman's Contra Corner

November 29, 2025

It should be damn obvious that the current blistering AI bubble is setting up Wall Street, the US economy and Trump-O-Nomics for a thundering bust. The AI frenzy has now gotten so out of kilter that fully $140 billion or 76% of the $184 billion gain in real GDP during the first half of 2025 was accounted for by feverishly surging investments in AI-oriented GPUs, network gear, server farms and data centers.

Moreover, this AI investment surge, which is expected to annualize to more than $425 billion in 2025, has been on a literally explosive growth trajectory. According to Grok 3, the comparable annual AI investment spending levels for 2022, 2023 and 2024 in the US were $104 billion, $179 billion and $250 billion, respectively. That is, the projected 2025 annual rate of AI spending will be up by 4.1X from just three year ago.

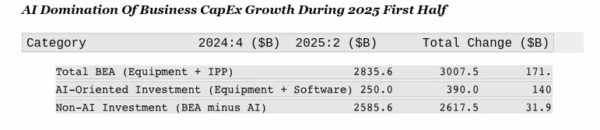

Of course, when you back out this AI investment explosion from the overall US investment spending numbers, what's left is pretty punk. To wit, non-AI investment in US equipment and intellectual property in the fourth quarter of 2024 totaled $2.586 trillion, which figure rose by only $31.9 billion as of Q2 2025. So the annualized rate of gain was just 2.4% during the 2025 first half-a level far below the 12.2% annual gain in the AI-swollen BEA figure for total US equipment and intellectual property (first line) investment.

In short, what is propping up the entire main street economy is an immense speculative surge in AI investment spending that isn't remotely sustainable because it's based on a fevered stock market bubble, fueled by the Fed's printing presses. And for want of doubt, let us remind what the real GDP and its major components looked like during the first half of 2025, excluding the AI investment eruption.

Annual Rate Of Change, Q4 2024 to Q2 2025:

- Real consumption spending (PCE): +1.54%.

- Government sector: -0.54%.

- Housing construction: -3.10%.

- Exports:-0.90%.

- Imports:+1.20%.

- Equipment and intellectual property investment, less AI: +2.40%.

- Business structures: -1.56%.

- Total Real GDP Less AI: +0.38%

So the question recurs. What happens when (not if) the AI bubble crashes. The sheer certainty of the latter is due to the fact that the runaway stock market is generating so much artificial capital that the AI-oriented hyperscalers are operating straight out of the playbook of the late 1990s dotcom bubble. That is, they are injecting huge amounts of capital into start-ups, smaller customers and linked vendors in their supply chain eco-systems, thereby enabling the latter to buy from these same high flyers massive amounts of chips, network equipment, other gear and software for data centers and server farms. NVIDIA, Microsoft etc. can then report soaring sales and stupendous profits. That is, until the bubble finally bursts.

Needless to say, today's AI spending eruption starkly parallels the fiber optics and telecom network spending frenzy during the dot-com bubble (late 1990s to early 2000s). Back then, telecom companies vastly overbuilt fiber-optic networks to meet booming anticipated internet demand, fueled by speculative valuations and easy capital. When soaring demand projections failed to materialize, many fiber suppliers, telecoms and network equipment suppliers ended up in bankruptcy or suffered severe stock price declines.

For want of doubt, here is a review of the major fiber-optic suppliers and related telecom equipment companies that were central to the dot-com era's investment boom and which also experienced bubble-scale stock price surges-only to crash spectacularly between 2000-2002. These firms supplied fiber cables, networking gear and infrastructure for the internet backbone.

Corning Incorporated...was a leading global supplier of optical fiber and cables, which were critical for telecom networks. Its stock peaked at $113 per share in September 2000 on the back of a doubling of revenues from $3 billion in 1998 to nearly $8 billion during the June 2001 LTM period. Thereafter, of course, revenues cratered back to $3 billion by December 2003, while the modest $550 million of net income that had been posted in 1999 plunged to nearly a $6 billion loss by the March 2003 LTM period. While Corning Inc. ultimately survived, the dotcom crash caused its employment level of 40,000 in 2000 to plunge to 20,000 by December 2003, while its capex level $2.1 billion per year at the peak fell to just $280 million by September 2003.

JDS Uniphase...was the dominant provider of fiber-optic components (e.g., lasers, transceivers) for network equipment. Its market cap hit $153 billion in 2000 on peak sales of $4 billion, thereby reflecting an absurd 38X market cap-to-sales multiple. During the following year sales plunged by 35% and the company was forced to book a $56 billion net loss which included $45 billion of goodwill write-downs on its extended string of over-priced acquisitions. Thereafter sales fell to less than $2 billion by 2002 before its remnants were merged into successor companies.

Lucent Technologies...was the Western Electric division spin-off in 1995 from AT&T. On the back of its monopoly supplier position in the Ma Bell system, Lucent had become the nation's dominant supplier of telecom equipment, including fiber-optic systems and switches. Its stock peaked at $84 per share after its pre-spin-off revenues nearly doubled to $38 billion by FY 2000. But when the tech bubble collapsed, revenues plunged to less than $16 billion, which generated huge losses and a 99% crash of its high flying stock to $0.55 and an eventual bankruptcy filing. Subsequent to its bankruptcy filing its remnants were acquired by Alcatel in 2006 after heavy losses.

Nortel Networks...was a key player in fiber-optic networking gear and telecom infrastructure. Its market cap reached $400 billion in 2000 based on peak annual revenues of $30 billion, again implying a still absurd market cap-to-revenue ratio of 13X. By the time of its bankruptcy filing in 2009, when its assets were mostly liquidated, revenues had dropped by 92% to $2.4 billion.

Ciena Corporation..... supplied optical networking systems for long-haul fiber networks. The company's stock hit $151 per share in 2000 and then fell to less than $5 by 2002 on the back of collapsing financials. Thereafter, the company required more than a decade to recover by focusing on optical transport products.

Global Crossing.....built and operated transoceanic fiber-optic networks. It was valued at $47 billion in 1999 before falling to less than $70 million. Upon filling for bankruptcy in 2002, its remnants were acquired by Level 3.

Level 3 Communications...was another major fiber-optic network operator and bandwidth provider. Its stock peaked at $132 per share in 2000. After dropping to $1 in 2002, it was reorganized in bankruptcy and later acquired by CenturyLink (Lumen).

In short, during the 1998-2000 boom telecoms were spending about $100 billion annually on fiber cables and internet infrastructure, expecting exponential internet growth. Suppliers like Corning and JDS Uniphase saw revenue spikes but overcapacity led to a crash when the hordes of dot-com start-ups and internet users failed. Consequently, global fiber-optic demand fell about 80% from the 2000 peak, with $2 trillion in market cap erased across telecoms and their suppliers.

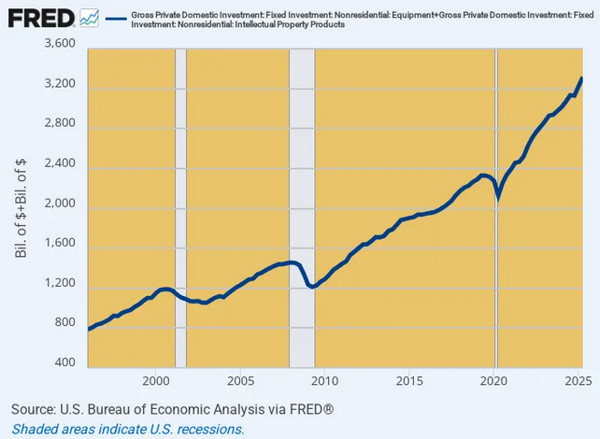

Needless to say, the crash in the telecom/internet capex sector left a huge hole in overall US fixed investment in business equipment and intellectual property. In constant 2003 dollars, business investment (excluding structures) had climbed by 33% from a $930 billion annual rate in Q3 1996 to a peak of $1.250 trillion by Q3 2000.

Yet by Q1 2003 total US capex in equipment and intellectual property had dropped by more than $200 billion. That is to say, when you take a -16% bite out of real capital investment even government stimmy spending is hard pressed to keep total GDP above the flat-line.

Of course, the associated drop in the stock market capitalization was even more dramatic. The aggregate value of the S&P 500 peaked at $12.7 trillion in March 2000, but then plunged by $5.2 trillion or -41% to $7.5 trillion at the September 2002 bottom.

Likewise, during the Great Recession collapse of 2008-2009, the S&P 500 peaked at $13.5 trillion in June 2007 and then fell by $6.6 trillion or -49% to $6.9 trillion at the March 2009 bottom.

But here's the thing, today's market cap of the S&P 500 is both far higher than in these earlier crashes, but also far more concentrated in the top 10 names, consisting heavily of the AI high flyers. Thus, at the present time fully 41% of the total S&P 500 market cap is accounted for by just 10 stocks, as we itemize below.

On the other hand, the level of market capitalization exposed to a potential meltdown of the AI bubble is an order of magnitude higher. The S&P 500 market cap recently weighed in at $56 trillion, representing another $4 trillion gain from the chart line shown below as of a few weeks ago.

Accordingly, the S&P 500 market cap is now 4.4X larger than it was at the dotcom peak and 4.2X larger than on the eve of the Financial crisis. Were the impending AI bubble crash to come in at an average of the two prior stock market meltdowns, a -45% plunge would shave $25 trillion of value from the stock market.

We think there is every chance in the world that the top 10 stocks which now account for 41% of the total S&P value will experience thundering meltdowns in the quarters ahead, taking the entire stock market with them. The degree of over-valuation is simply out of this world, starting with NVIDIA Corp which despite its recent tick down is still capitalized at $4.6 trillion or 28X LTM sales.

This valuation is just plain bonkers, even if AI turns out to be the greatest invention since sliced bread. Critics note that 2025's estimated $475 billion of global AI capex dwarfs actual AI- based revenues, which amounts to $3-5 billion at best. That is to say, there is as of yet no return on capital investment in sight, thereby risking a similar "dark pool" of unused capacity that plagued the telecom world after the dot-com crash.

Needless to say, a collapse of the AI high flyers would also have a thundering impact on capex spending for equipment and intellectual property, which is the only thing holding real GDP above the flat-line. Again, the current scale tells you all you need to know:

- Dot-Com Crash: Capex of $1.189 trillion in Q4 2000 dropped by -$136 billion or -11.4% by Q1 2003.

- Financial Crisis: Q1 2008 peak spending for equipment and intellectual capital of $1.457 trillion, plunged by -$245 billion or nearly -17% by the Q1 2009 bottom.

- AI Boom: The current annualized run rate of equipment and intellectual property spending of $3.316 trillion is so extreme that it could readily drop by 20% in a downturn-especially given that AI spending of $425 billion this year represents an 100X gain since 2022. Yet a 20% reduction would result in a -$650 billion investment spending plunge--a figure way off the charts of prior history.

US Fixed Investment Spending For Equipment and Intellectual Property, 1996 to 2025

It goes without saying that a $650 billion decline in capital spending would also plunge the already struggling US economy deep into the recessionary drink, and do so at a time when there is no policy margin for error. That is to say, fiscal policy is already tapped out with $38 trillion of public debt and the Fed's printing presses have already implanted 40 year high inflation in the price level of the US economy.

We'd say that what is coming down the pike, therefore, does not look much like the ballyhooed Golden Age the Donald and his MAGAphones so foolishly expect.

Reprinted with permission from David Stockman's Contra Corner.