RADHIKA DESAI: Hi everyone. Welcome to the fifth Geopolitical Economy Hour, the fortnightly show about the political and geopolitical economy of our times. I'm Radhika Desai.

MICHAEL HUDSON: And I'm Michael Hudson.

RADHIKA DESAI: So this is our third and final show on the theme of de-dollarization, based on our work, particularly on Geopolitical Economy that I wrote in 2013 and Super Imperialism that Michael wrote some decades ago and has recently reissued.

Based on my Geopolitical Economy and Michael's Super Imperialism and also of course our article which we co-wrote called "Beyond the Dollar Creditocracy".

As many of you know we have structured our discussion around some ten questions.

So as you see in this slide they are all here. In the first show we answered the first five questions. In the second show we answered the next three, which are, How did the Sterling system end? What really happened between the wars? And, How did the dollar system work between 1945 and 1971?

So in this show we are going to take up the last two questions, which are: Was there really a Bretton Woods II really after 1971? And finally, What is the crisis today - what are its main dimensions?

So that's what we're going to do. So let me just start off by just saying one thing about the first question, which is, Was there really a Bretton Woods II after 1971?

Now the most important thing to know about this is that the very label "Bretton Woods II" involves a boast. And let me also explain that by pointing out that actually by calling it a boast I'm drawing attention to a very important fact about the whole discourse around dollar hegemony and so on.

And that fact is that there is an absolute industry of writers - on the dollar and dollar hegemony and US hegemony and so on - whose business it is to constantly talk up the dollar. No matter what's happening on the ground, the conclusion they draw from whatever is happening is that the dollar system is here to stay and here forever.

And so if the dollar goes up they say, "Oh look, the dollar is high and everybody wants the dollar." If the dollar goes down they say, "Well, see, people want the dollar even though it's down."

So this is the kind of weird reasoning that you see, and of course Michael and I have unpacked a lot of it already, and in this show we will continue to unpack it.

So basically the boast about so-called Bretton Woods II - that is to say, the dollar system after 1971 - is that this was "hegemony without tears". That the United States had been freed from the burden of linking the dollar to gold.

Michael I think you have some points on this as well.

MICHAEL HUDSON: Well the United States aimed to not lose any more of its gold, because gold is how it had bouldered its control over international finance since the 1920s.

The US also wanted to keep its veto power in the IMF and the World Bank. And it's continued to be led -the World Bank certainly - by US military strategists, and the IMF has in fact just continued American foreign policy.

So the story is that what was new is that the United States was able to pay in IOUs - Treasury securities - and which now we all know really are never going to be paid because they can't be repaid, anymore than the government is going to retire the paper currency, the dollar bills that you have in your wallet.

The irony and the internal contradiction here, is that this success in maintaining American power and American policy enabled the United States to become, well we can just say it, parasitic. It enabled it to deindustrialize.

It enabled the United States to get so much revenue from its foreign investments, from its foreign lending, and from its control of the foreign trade system and the tariff system, that it was able to deindustrialize and actually become dependent on other countries for essentials. Just the opposite of what it had tried to make other countries do.

And this was a kind of poison chalice. It left the United States in what we now know is an untenable position.

How can it live off the surplus exports and payments of others while it itself is being deindustrialized? What is the basis for its power if not ultimately military?

Any breakaway from the US economy is going to leave it isolated, as we now can see, and unable to provide for its own basic needs. So it needs to have an international financial system that actually works as a kind of neo-colonialism, a neo-imperialism. You can call it financial colonialism and financial imperialism. And that is driving, right now, other countries out of the US orbit as we've talked about today.

And their withdrawal isn't simply from the dollar as a currency, it's from the foreign trade system, the foreign investment system, and the foreign debt system that the United States has used since 1971 to bolster its international position.

RADHIKA DESAI: So exactly, Michael. You know it's really important - we both tend to emphasize in our writings and our writings together that this is the key.

If you want to run a system like the dollar system, what you're going to do is exact a price from your productive economy. You're going to deindustrialize it. You're going to make it weaker.

Now if the US economy has become reliant - and particularly of course the US elites, the US ruling classes have become reliant - on an introductive predatory speculative financial system. And if that financial system, on which the dollar is based, is essentially unraveling, then you can easily see that the United States is in for a rather big crisis, a rather big reckoning. And it's gonna be hard.

But let me say one other thing very quickly.

The United States has always, as we've emphasized in previous shows - this whole desire to install the dollar as the world's money comes out of a certain interpretation - a certain wrong interpretation - that American foreign policy elites have made throughout this period, going back to the early twentieth century, about how the sterling system ran.

They simply did not did not see that the sterling system ran on the basis of empire. But they have sought to emulate that without an empire. And even with an empire the sterling system was not sufficiently stable, and the dollar system is even less so.

But the important point is that, as soon as the UK started essentially running the sterling system, it also set the stage for the deindustrialization of the UK. And you are seeing a repeat of that process a century later in the case of the United States. This is really quite a serious point.

So I think we've given you a broad conception of the contradictions. But it tells you also why we need to look at the reality of the dollar system and its contradictions.

Because you see if we're going to talk about de-dollarization, then if we don't understand how the dollar system was contradictory, we will think of de-dollarization as something that has hit the dollar system out of the blue.

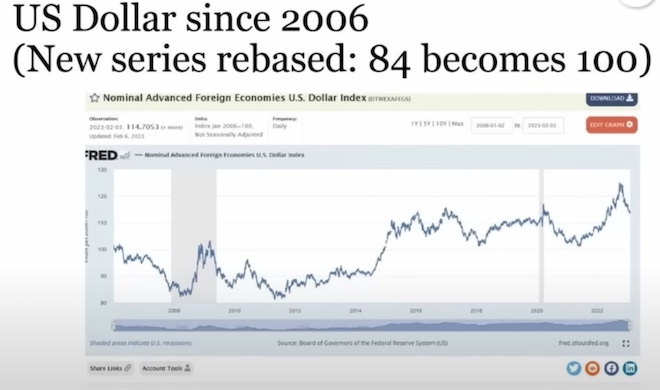

In reality it is the maturation of the contradictions of the dollar system. And if you see, for example in the next two slides, I'm just going to show you the value of the dollar declining. So Paul if you will show - yes the dollar since 1971.

You'll see here that there is a huge rise in the dollar in the early 1980s, which is the Volcker shock. And since then you see, although there are ups and downs, there is a secular downturn in the value of the dollar. With the stock market bubble the dollar went up. But funnily enough, all the money coming into the United States after the housing bubble, all the money that was attracted into the United States -massive quantities of money - were not able to prevent the downward slide of the dollar.

And since then, quantitative easing, etc. quantitative easing one, two - quantitative easing infinity, etc. - have let the dollar go up, but now you see what they began to do in the last decade or so, is they have rebased the whole system.

So the two peaks here that you see - in the previous graph they are valued at about 80. And in the new graph, you see that they are valued at about 100.

So they basically are basing the dollar up again so you do not see the broad secular decline, but believe me, there has been a secular decline in the value of the dollar.

And this is despite all the efforts made by the Federal Reserve to essentially run the casinos of various asset bubbles which would have brought money into the dollar and therefore kept the value of the dollar up.

Because remember, our argument has been - my argument in Geopolitical Economy, Michael's argument in various writings, and also our argument in "Beyond the Dollar Creditocracy" - is that, since 1971, essentially the United States has sought to make the dollar system function by counteracting the "Triffin dilemma" effect.

By expanding purely financial demand for the dollar. Not economic demand, not investment demand, not trade demand, but purely financial speculative demand for the dollar.

And this system essentially is now unraveling. And just to remind everybody, the Triffin dilemma is simply the assertion of Robert Triffin going back to the late 1950s when he pointed out that the United States's effort to try to provide the world with liquidity by running deficits was essentially deeply contradictory, because the more liquidity it provided - therefor the greater the deficits - the greater would be the downward pressure on the dollar.

And many people - especially those who are part of the industry of the dollar boosters - they hate talking about the Triffin dilemma. And if they ever talk about it they say, "Oh well, after the dollar's link to gold was broken it's no longer operating."

That has simply not been true. It has continued to operate, and the United States has made great exertions - and we will discuss them all in some detail now - but it has made great exertions to try to counteract this effect. Particularly by, as I say, allowing huge speculative bubbles to be inflated in the dollar financial system, so that investors, speculators would bring funds into the dollar system so as to keep demand for the dollar up.

So that's the key thing. The Triffin dilemma never stopped operating. And 2008 was a big peak for that.

MICHAEL HUDSON: Well by 2008 what's important is that what we've called dollarization was really what the US State Department called the "rules-based international order." Meaning, rules that it's set.

By 2008 almost every country had managed to extricate itself from the International Monetary Fund (IMF). I think [Türkiye] was the only country that was still remaining as a client of the IMF because it was widely recognized that the IMF "medicine" of austerity actually is a kind of poison, it's not medicine at all.

And the World Bank's idea of "development" was basically underdevelopment. It was basically dependency on the United States exporters - especially its farm exports - and creditors. Instead of creating their own money, instead of producing their own food, instead of producing their own products.

What Triffin neglected to point out is that the US deficit - he isolated that from the whole world system, and the world system was designed to make other countries dependent, and that was why the dollar didn't go down anywhere near what Triffin's so-called dilemma implied. Because the dilemma was solved by what we're calling monetary imperialism.

RADHIKA DESAI: Yes. So you know one of the other broad realities that we have to look at is that in this period - that is to say the period since 1971 - the United States financial system, which had been made into one of the most highly regulated financial systems thanks to the Depression-era regulations that were brought in in the 1930s - and therefore this financial system had been kept focused on productive investment - in the period since 1971 you see its gradual transformation into a financial system which is the opposite of what a really productively dynamic country needs.

In any case, the dominant story - the story told by the dollar boosters - is that after 1971 the dollar played this world role without having to bear the burden of being linked to gold, without having to exchange dollars for gold. It was sort of like a hegemony without tears.

But actually when we look at what happened you see a very different story.

So immediately, once the dollar's gold link was broken, it plummeted. And again, the story told by the dollar boosters is - they always try to make everything look as though it's all under the United States' control. So when the dollar plummeted they said, "Oh it's great for the United States. United States exports were competitive."

But if it was so great, then the United States monetary authorities, the Federal Reserve, would not have intervened in markets in order to shore up the dollar. And we know they did.

So the point is that these interventions show that actually the dollar was plummeting far more than what the US authorities had required, and that simply allowing the dollar to "find its own level" without backing of gold was no easy ride for the dollar.

MICHAEL HUDSON: Well they were sort of trapped by their free market view that really was their form of market intervention.

All markets are regulated, any kind of a market. Either they're regulated by governments, or by monopolies, and by bankers. And the free market economists who are saying, "Oh, it's wonderful, we've been able to not only go off gold but in the process we've devalued."

And Treasury Secretary [John Bowden] Connally was pointing to the fact that now we can really get an advantage for our exporters, not realizing that pretty soon we were going to deindustrialize and not really be an export economy in the way that we were before, because we were becoming a very high-cost economy.

A high-cost economy because of our military spending, because of the increasing financialization, by the fact that more and more of the income in the American economy wasn't going to the expert sector of products at all. It was going to real estate and finance and was becoming the kind of economic overhead that has undercut America's ability to export, and therefore it undercut its ability to balance its international payments by trade as we're now seeing.

So the United States tried to control world trade and investment markets via the financial sector backed by diplomatic brass knuckles. And that was the reality that the country has been trying to deal with.

RADHIKA DESAI: Absolutely Michael. This myth people talk about - how markets are somehow spontaneous and natural and so on. All markets are made. They need a whole panoply of government regulation in order to create a market for anything.

And this goes also for the international market for dollars. You know, again, there are the dollar boosters, the people who want to say that the dollar system is completely natural and has no problems and will last forever.

These are the people who always argue that the creation of the so-called "Eurodollar market" - that is to say a market for dollar and dollar-denominated financial instruments outside the United States - [they would say] "It had to happen because you can't control flows of money. Money flows out inherently uncontrollable."

Of course, if they were inherently uncontrollable, then why would the United States and other such governments spend so much time and effort trying to persuade countries to lift capital controls?

Because capital controls actually work, and they don't want these capital controls to work.

So anyway so the point I'm trying to make is that the Eurodollar market itself was a result of changes made to the legal and regulatory environment in which money operated, both domestically and internationally, particularly in the United States and the United Kingdom at this time, which laid the basis for the creation of an international market in dollars.

So anyway, the first point is that the fact of the matter is that United States authorities could not afford to accept whatever valuation the market gave to the dollar. They intervened in markets to try to shore it up.

The next thing that happened is also really interesting. Which is that essentially the dollar was falling so much that commodity prices were also rising. Or commodity prices were rising.

You see, any money has - and the dollar in particular - has a very specific relationship to the prices of commodities. They move in opposite directions. If commodity prices go up, the value of the dollar goes down.

So one of the things that happened in the late 1960s and early 1970s is that there was a big rise in the prices of commodities in general. And if you see in this chart it shows you that there was a big spike in the prices of food in the early 1970s. And partly in response to this - but partly also because the dollar was falling - the OPEC countries - the newly formed Organization of Petroleum Exporting Countries - basically jacked up, in 1973 they quadrupled the price of oil.

This was a really earth-shaking event in its time. It was destined to have extremely bad consequences for the world economy, and a large part of what began to happen from hereon was the United States intervened in this crisis in order to once again use the crisis as an opportunity to stabilize the dollar.

MICHAEL HUDSON: During this period I was going back and forth to the White House with Herman Kahn regularly to talk to the Treasury Secretary and the staff that was drawn largely from the oil industry.

And the US told the oil countries that they could raise their export prices as much as they wanted. The more that OPEC would raise its oil export price, the larger the price umbrella became for American oil companies. So the American oil companies were very glad to see this, because it certainly helped.

All the United States wanted from the oil countries was, "All of your export earnings have to be sent to the United States by buying US assets headed by Treasury securities or minority stock ownerships and bonds."

And some of the Saudi oil sheiks were said to buy a million shares of every stock listed in the Dow Jones Industrial Average. So there was a huge flow, not only into US Treasury securities and other securities, but also into American banks and British banks.

You mentioned Eurodollars. And the United States preferred for deposits to come to the United States via London Eurodollars. Because when I was at Chase we found the single largest foreign depositor was really the young twenty year old who was in Chase's London branch who was in charge of sending the Eurodollars to the head office in New York.

The Federal Reserve rules said that banks didn't have to have any reserve requirements against Eurodollars, unlike deposits. Eurodollars were the way in which the United States got sort of free money for the bankers. And the bankers were flooded with these dollars, on which they paid very low interest. And they turned around and began lending them out to Global South countries - to Latin America especially, to Africa, to Asia.

And so this money flowing in became an almost reckless re-lending of these dollars to Third World debtor governments.

RADHIKA DESAI: So the first thing I should say here of course is that this was a very complex moment, and there were certainly advantages of this moment - the quadrupling of oil prices - for the US because in part of course the US itself had big oil companies which were of course happy to benefit from it.

And the other thing that this did of course, is that by raising prices of oil and ensuring of course that and still dominating it in dollars, meant that the rest of the world now acquired four times as many reasons to hold dollars.

So again this in itself played a role in stabilizing temporarily at least the value of the dollar.

But at the same time, as Michael said, the Americans basically persuaded the OPEC countries to deposit their money in Western financial institutions, US financial institutions, particularly those based in London but elsewhere as well.

And they of course had to go on a lending spree. Because remember, it may sound like a great thing that you are a bank and all these people are depositing money into your bank, but the fact of the matter is, if you're a banker, if people are depositing money into your bank, you've got to pay interest.

Where are you going to earn the money to pay interest from? You can only do so by lending. And that's why you see this enormous lending spree, as Michael says without really taking account of the consequences.

By the way there was also a big lending spree within the United States. There was certainly a big international lending spree and money was lent to Third World countries and also communist countries where necessary.

So in this period there were very complex new processes of money flows that were set up. And in this context the other thing that began to happen is that for many Third World who were borrowing this money, they were getting access to this money practically free of charge, in a sense, because in the 1970s again, nominal interest rates, wherever they were, but they were not low, they were relatively high, but so was inflation.

So in real terms, there were actually negative real interest rates, and this as I say created a spigot of practically free money for Third World countries to borrow and to industrialize with.

Yes, many Third World countries also - this money flowed into corrupt bank accounts and so on - but many Third World countries were also using this money to industrialize. And in the end, this is not something that the United States wanted to see, because from the start the United States has always wanted to have its relative power unquestioned, not just its absolute power.

So in that sense, this whole scenario had very mixed consequences. The United States continued to experience very high inflation, and therefore the pressure on the dollar continued, and lending was flowing out to Third World countries who were also industrializing. So the scenario was not great.

And in this context let me also say that another problematic thing from the US point of view is that European governments had already forced the hand of the United States into breaking the link with gold, because essentially they demanded so much gold, and they acquired so much gold as the consequence of their export surpluses, that it left the US with no choice.

Now, immediately after the breaking of the link with gold, the United States and the European governments were involved in the so-called "Committee of 20" which was supposed to try to find a solution to this crisis and essentially try to negotiate a new financial system.

And in this again, Keynes's ideas were brought back on the table and so on. But the United States essentially brought to an end the Committee of 20 negotiations by doing this deal with the OPEC countries and changing the situation on the ground.

And by the way, that deal with the OPEC countries also involved something else. Western Europe and Japan, as the capitalist allies of the United States, were heavily dependent on importing oil. And they were desperate to try to create a sort of multilateral recycling of petrodollars in such a way that they said to the OPEC countries, "Look, it's your right, it's your oil, you are free to raise the price of oil. But at least let's create a system in which we can borrow from you the money we need. Essentially give us your surpluses as export credits."

And this possibility was nixed by the United States, and that's how you got this recycling of petrodollars through Western financial institutions.

So once the Committee of 20 negotiations were essentially scuttled by these means, the Europeans were essentially quite mad, and they said, "Ok, we are going to start our process of monetary integration" - something that they had been talking about for a while. But they now took the first steps in European monetary integration which would eventually lead, almost thirty years later, into the creation of the euro.

So this is also very important, because people fail to see this, but the euro itself constitutes the first example of exit - a planned exit from the dollar system. Because by creating the euro, the European countries essentially ejected the dollar from their mutual transactions.

So for trade within the European Union, etc., not only initially European currencies and eventually the euro were really what were going to be used. So this was the beginning of European monetary integration.

MICHAEL HUDSON: I want to say what was happening in the banking sector.

The government wanted the banks to find it profitable to accept the oil OPEC deposits. When I was working at Chase in the 1960s, my job was to analyze whether countries could pay or not. But by the 1970s, I had a meeting at the Federal Reserve and they said, "You don't need to analyze the ability to pay anymore. Because if a country can't pay its debt to the United States, we will lend that country the money."

And I said, "I don't see how" - and I named some Latin American countries, Argentina and Chile. "How are they going to be able to pay?"

And the Federal Reserve officer said, "Well according to your analysis, Professor Hudson, England is insolvent. It can't pay."

And I said, "Oh I'm glad you mentioned that. Yes."

And they said, "But is it going to pay? Of course it's going to pay. We will always lend England the money to pay the money it owes the United States. It'll just be indebted to us." And you were going to do the same for Latin America.

So the American Banks were encouraged. They said, "Okay, we don't have to look at the markets anymore. We don't have to do an analysis of the ability to pay. The whole system has become political."

Well, since you bring up the creation of the euro, Radhika - the euro was indeed meant to integrate the European economies, largely by combining the surplus run by the German economy, with the rest of the Eurozone that was running a deficit.

And so in that sense, they were trying to balance and stabilize their own exchange rates. However, the way in which the euro was created was basically the satellite currency of the United States, because it was designed by Robert Mondell at the University of Chicago for what he was given the annual Nobel Prize for the worst economic advice that they give annually.

And he created the euro in a very right-wing "Chicago School" way, in a way that blocked the Eurozone from actually using the euro and the central bank to actually finance Keynesian-style budget deficits.

European countries were forbidden to run a budget deficit of more than three percent of their GDP, which is a very small amount. And what that did was prevent the euro from creating enough money, enough currency, enough credit, to really become a rival for the dollar.

It was sort of crippled from the very beginning by the rules that made sure the government would not be able to create enough credit to enable European recovery to take place without very very heavy borrowing from the European banks and from the American banks.

So the euro was created in a way to minimize the role of government, maximize the role of banks, and essentially that's what made it a right-wing Chicago School development from the very beginning, and we've now seen how it's unfolded.

RADHIKA DESAI:YOu certainly are absolutely right, Michael, when you say that the design of the euro is quite right-right. Although I would attribute it - although there's also no doubt that the advice given by Robert Mundell was certainly part of the thinking of the Europeans when they were designing the euro.

But I would say that also the ideas that flowed into the creation of the euro were as much a result of German older liberalism which has always been exceedingly monetarily conservative.

MICHAEL HUDSON: Yes.

RADHIKA DESAI:So in terms of the ideas, there is also another thread of ideas pouring into this. In terms of the kind of financial system it created, I think this is also a really interesting thing because, on the one hand, the euro was designed - as you rightly pointed out - to preserve the dominance of the German industrial machine in Europe as a whole.

And then for the rest of the countries of Europe, with these sort of limits on deficits and so on, it was designed in such a way as to penalize them for engaging in any kind of productive expansion of their activities, and that's also true. But that's really more having to do with the internal politics of the European Union and the dominance of the Germans in the project.

And of course, remember, this project evolved over a very long period of time.

But having said both of those things, and agreeing with both of those things, I wouldn't go so far as to say that the result was that the euro became a satellite currency of the US.

The fact of the matter is that the euro did - the whole process of European monetary integration and eventually the euro - it did take the mutual transactions of the Europeans out of the dollar system. It made them independent of the dollar system.

And also, the euro is used more widely.

What you are pointing to, which is the way in which the United States financial system provides credit and functions on the basis of deficits - yes, that is something the euro is not going to do.

But that again goes back to our contrast between a productively-oriented financial system and a speculatively-oriented financial system, and we will come back to that when we come to this later.

But yes, so definitely the euro was created certainly as a way of essentially the Europeans stepping out of the dollar system.

Now, we are still in the 1970s and another thing that I would like to point out and remind people of, is that the mid-1970s is also the period when the G7 meetings begin. Originally the G6 and then the United States brought in Canada as sort of ao North American partner. And this made it the G7.

And the G7 meetings, which are annual, were forums where a lot of the extremely fraught politics of the dollar were played out. Where the Europeans, for example, would demand that the United States reduce its deficits, and so on.

And now remember they no longer needed dollars. So they kept saying the United States should reduce these deficits. They also put pressure on the United States to stop the war in Vietnam which was proving very inflationary.

They essentially ensured that [Lyndon B]. Johnson would refuse to run for a second [presidential] term because they made it politically impossible, and people even said this was the Europeans dictating to the Americans.

So essentially the G7 became a forum at which the mutual exchange rates and so on would be determined based on collective decisions. So this idea that somehow the United States was running its own show, unilaterally deciding monetary policy for the world, this is simply has never been true. Certainly not as long as the G7 has been operating.

And so in that sense, you also see the depth of the crisis of the dollar system that you found in the 1970s.

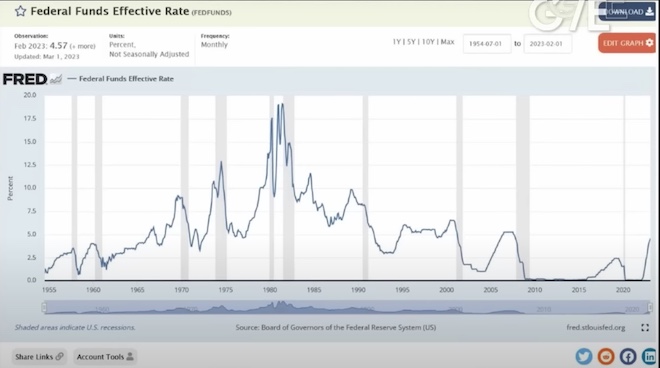

And this crisis appears as though it is resolved by the Volcker shock. And essentially this is the point where in the late 1970s inflation is going out of control in the United States and Paul Volcker, who is regarded as a "sound money" man, is brought in as the new Federal Reserve chairman in order to deal with this problem.

And Volker does the only thing that capitalist country central banks know how to do - which is, the only way they know how to deal with inflation is to restrict money supply, and allow interest rates to rise as high as they want, a particularly rise above the rate of inflation, so that eventually by rising high enough they will create a recession and they will eventually - the recession will kill inflation, rather than any particularly deft monetary policy,

So this is what he did in 1978-79.

Well Volker was my old boss's boss at Chase Manhattan, and I was the note taker on talks that he would give periodically to the banks. And when you say he was fighting inflation, he defined inflation as "what construction workers are paid."

And he said, "I'm going to raise interest rates until I don't see the wages of construction workers rising anymore."

And they rose to a peak of twenty percent in 1980. And the important thing is that obviously with interest rates that high nobody could borrow to buy housing - you're not going to pay a mortgage at twenty percent rate over thirty years. Companies couldn't borrow.

But what this did was crash the stock market, the bond market, and the real estate market, by the interest rates.

This set the stage for the Reagan decade, for Reaganomics. This set the stage for the largest bond rally in history.

Interest rates went down from twenty percent then to I guess you could say last year's almost zero rates. There was a steady decline in interest rates, a creation of enormous interest credit and basically the banks were given enough money that all of a sudden the way to make money after Volcker was not by industry anymore.

It was by financial means: by corporate takeovers, by the leveraged buyout - all of that became the legacy under Reagan, combined with tax cuts for the financial sector, tax cuts for the high income people, but most of all the financialization of industry the transformed the whole role of the US economy in international affairs.

RADHIKA DESAI: Before we - and this is a really important point Michael - but I also want to say one other thing about the Volcker shock before we move on to what this did to the US economy, which is something very serious and important for us to understand.

But the Volcker shock, by allowing interest rates to go as high as they did - and at one point they hit nearly twenty percent in the United States, right - so this is how high interest rates had to those days to essentially bring down inflation. As Michael said [Volcker] defined it particularly in terms of wages, and that's definitely also important.

But this sort of Volcker shock created the Third World debt crisis, beginning with the default of Brazil, Mexico, and Argentina. And this is also very important from our point of view today, because, again, first of all, the fact that the Volcker shock created the debt crisis, the fact that the dollar went up very high in this period - again this is used as grist for the mill by those who are boosting the dollar.

But in fact it is actually - this whole process was creating many contradictions.

As far as the Third World was concerned, it did look as though this was the United States not only bullying the Third World and oppressing the Third World but also getting away with it.

And certainly the 1980s and 1990s were periods during which, thanks to the Volcker shock and the Third World debt crisis, many Third World countries actually experienced a retardation in their growth. They had to work harder and harder to produce more and more of the cheap goods - whether it was coffee or cocoa or cotton goods or cheap manufactures or whatever it was that they were producing - they were producing their guts out in order to export to the rest of the world, particularly to the First World countries, in order to earn the dollars to repay the debt.

So this debt was being repaid. And of course, the fact that they were repaying the debt was also bringing fund flows into the dollar system. But this sort of dollar repayment was really repayment by punishment. It was a repayment by restricting consumption by Third World countries - consumption as well as investment in Third World countries - rather than repayment by increasing the capacity of these countries to produce.

And of course the whole process was overseen by the World Bank and the IMF. So when Michael says that these institutions were actually promoting underdevelopment rather than development, you saw that in all its gorey details in the 1980s and 1990s. So this was really quite important, what happened to Third World countries.

And by the way, this also meant that the price of everyday things that you could buy in a First World country, whether it's tea or coffee or cocoa or shoes or what have you, began to go down.

So it looks like this is a great victory for the United States. But now let's look at what this did, what the policy priorities set in train by the Volcker shock - which are essentially the policy priorities of neoliberalism - what they did to the productive apparatus of the United States itself.

Because the Volcker shock punished US industry.

US industry was already beginning to decline, particularly relative to the more robust productive and technologically advanced industries of Western Europe and Japan. So US industry had already begun its decline in the late 1950s and through the 1960s.

But now that decline is massively accelerated. And what you see, already by the first couple of years of the Volcker shock, you begin to see the end of the manufacturing interest as an independent interest. Let me explain what this means.

The Volcker shock basically induced a recession, and the recession was a double-dip, or double-u shaped, recession, so it extended over several years.

and in the first few years there was a manufacturing industry. These people got together, they went and talked to Reagan, they talked to Volcker, they pleaded for a lowering of interest rates so that they could continue industrial expansion and so on. But they eventually failed.

and what this also did is, when they failed, they essentially threw in the towel. They said, "If we can't make money by producing, we are going to try to make money through financialization."

So this set in process the financialization of many productive American corporations.

This is how - you may read in many places, a company like GM today is probably going to make more money by lending you money to buy their cars, rather than by making their cars.

So this was the beginning of the financialization of the US economy, and the end of an independent manufacturing interest.

MICHAEL HUDSON: Well, you've described two parallel forms of deindustrialization.

I was to review just what you said about the Third World countries.

Mexico defaulted in 1982. It could not pay the interest on its Tesobonos. All of a sudden, the high interest rates that were created at that time were not renewed. A lot of Third World debts were falling due, and they couldn't re-borrow these debts at three or four or five percent. They were charged huge amounts. All they could do was default.

And the defaults spread rapidly through Latin America, Asia, Africa. So literally the international bond market dried up, almost totally. No one could borrow in the 1980s. and we've discussed that on earlier shows.

So, without borrowing, how were these economies whose economic development had been crippled by the IMF and the World Bank - how were they to develop?

The only way they could balance their payments was to do what the US State Department told the IMF to tell them. "Sell off your industry. Sell off your public ownership of utilities, of basic natural monopolies. Your oil, your minerals."

So there was a huge selloff, and there was no money at all under the austerity of the 1980s for the Third World countries to really develop.

But what happened in the United States was similar! As Radhika just said, the money was to be made financially, not by actually investing in corporations.

This was the decade of junk bond takeovers, leveraged buyouts - initially by Drexel Burnham [Lambert] that began really with the CVS leveraged buyout, and then spread to the Nabisco [takeover] that was described in the book Barbarians at the Gate: The Fall of RJR Nabisco (1989).

All of a sudden, people could borrow - go to Drexel Burnham and later other houses - and borrow high interest rates - junk bonds. And at that time, eleven, twelve, thirteen percent was a bonanza for investors.

And how could they make money by borrowing at rates that profit-making industrial companies had never been able to do.

Well, they made essentially money by a kind of arbitrage. By borrowing at twelve percent, and buying a company whose dividends, now that the Volcker shock had collapsed the stock prices of industrial companies, they could borrow and buy assets, paying dividends at much higher rates than twelve percent.

And if they were not actually generating profits to pay these rates, they could begin to sell off the companies. They could carve them up. Companies were being bought out, broken up - [Henry] Kravis and KKR and all sorts of other companies were doing this.

And in fact it was free money for the investors, because they organized a criminal conspiracy, for which Drexel Burnham people and their clients, such as Ivan Boesky, were sent to jail.

Suppose you wanted to buy a company with borrowed money. Well, you'd get together and say, "Ok, in order to buy this company, we have to make an announcement of a takeover demand. And we're going to have to pay twenty percent, twenty-five percent, over the existing stock market price in order to have the existing stockholders say, 'Ok, we're going to sell out our stocks and you can take the company private.'"

Well, knowing that they were going to make a tender offer (unintelligible) - about twenty percent gain, which is a huge gain. Imagine making twenty percent in one week and only putting down five percent of the money yourself and borrowing from a bank or a brokerage house ninety-five percent for a stock option.

The Drexel Burnham investors would say, "We're going to buy Company X. But we're going to buy stock options to buy at this low price from existing brokerage houses." And then they'd make the tender offer - knowing how much they were going to offer - and the stocks would jump twenty percent. They would then exercise the stock options - at an enormous gain - and the stock options would give them the money to pay the stockholders to buy out the firm.

They became instant billionaires, and of course the feds finally said, "Wait a minute, this is insider dealing. You're not allowed to do this on margin." And they stopped that.

But what they didn't stop was the whole concept of leveraged buyouts and takeovers - of buying a company, not to, say, produce cars; not to produce toothpaste or consumer goods; but to produce dividends, and to produce rising stock prices.

Money was made no longer by making profits that would increase the stock price. For one hundred years, people had analyzed investment in industrial corporations by saying, "Let's look at the profits. Let's see how they're going up over time. And we're going to capitalize the value of these profits into stocks."

But what the takeover people did - the financial people - was say, "Well, we're not going to invest in making profits by the long-term investment, research and development, developing markets - that takes too long. What we're going to do is use the existing profits that we have to buy our own stock. Stock buybacks. And to pay dividends. We're going to raise the stock market price."

"And what we're producing is capital gains. Because the government is taxing capital gains at only a fraction of profits. The government tax system doesn't want people to invest in employing labor. They don't want companies to invest in capital expenditures to produce more. They want companies - and have designed the tax system - to make companies simply use the existing profits for stock buybacks and dividends and essentially shrink the companies. They want the companies to commit industrial suicide."

And indeed, Wall Street understood exactly what was happening, and they became - ever since the Reagan administration - participants in this industrial suicide of the United States by financializing the company, replacing industrial engineering with financial engineering, and essentially transforming the whole character of capitalism itself - away from industrial capitalism to finance capitalism.

RADHIKA DESAI: Yes, exactly, Michael. If you really count the cost that the United States economy has been paying, in order that the Federal Reserve, and other US authorities essentially create this international casino, which is the dollar system - if you count that cost, you really begin to see how the United States economy has come to such a (unintelligible) state.

And this is directly connected with the desire to keep the dollar as the world's money. Because throughout this period, while this is happening, essentially financialization is strangulating US industry. And even as it's doing that, throughout this period what you see is that, as the old, highly regulated financial system of the United States is coming under pressure because of high inflation and high interest rates and all sorts of things are going wrong.

Savings and loans were essentially - because they had lent for a long-term basis on long mortgage rates that were at very low interest rates, they were hit really badly by the nominally high interest rates and the high inflation of the 1970s. And they went into a huge crisis in the United States.

But if you examine what happened to that and how the authorities responded, what you see is something that has been true for the entire period since the 1970s. And that is that every time there is any problem with the financial sector - and there were many during this time - instead of saying, "Let us re-regulate - the old regulations are not working, but let's put in new regulations which will try to achieve the same aims." - Instead of that, they always deregulated in a way that encouraged financialization. That is to say, the increase in financial activity in relation to productive activity.

And of course increasingly that financial activity no longer serving to expand production, but rather serving only to suck out the profits that were being made, whether in the form of profits or wages by productive forces - whether productive capital or workers.

And what's really interesting as well is that this entire period - if you see the slide that that shows interest rates through the entire period - you see here the interest rates of course reached a peak in the Volker shock of nearly twenty percent. And then you see them coming down. But what you also see - and of course you see in the present time since the 2000s, you see them exceedingly low as well - but what you see in the 1980s and 1990s is that this was a period of financialization in which interest rates remained relatively high.

In themselves, these interest rates would have made it very difficult for that to be a revival of US industry. So in this period you had essentially high interest rates strangulating US industry.

MICHAEL HUDSON: Well while these interest rates were falling, they still remained high. And as they fell, the economy could afford going deeper and deeper into debt.

This is what the business cycle theorists missed.

If you look at typical discussions of the business cycle, it's a cycle. Like a sine curve, smoothly going up and down.

But what was happening, especially since the 1980s, is that each recovery - and we've said this before in this show - each recovery since World War II has taken place at a higher and higher and higher level of debt.

So the economy was gradually increasing its debt, because that's how wealth was created. It wasn't being created by capital investment in industry. It was created financially, mainly by debt leveraging, by borrowing money at interest and making a capital gain on it.

The result is that people thought that the economy was getting richer and richer, but this wasn't an industrial business cycle, as people had discussed before. It wasn't a cycle of costs and prices going up and down and automatic stabilizers. There was nothing to stabilize the exponential growth in debt that was taking place.

So the result is that as you could make money financially, instead of by industrial engineering and production, you had the economy deindustrializing more and more. And all of this was depicted as creating wealth.

It was creating financial wealth, not industrial means of production or what people had usually thought of as being tangible, real wealth.

The byproduct of all of this wealth is that it was very heavily concentrated in the wealthiest 1% - maybe 10% - of the economy. This financial wealth was not shared with the participants in the industrial economy of production and consumption. And so the economy was being distorted. Its shape was shifting. It was polarizing.

The wealth of the 1% really found its counterpart - on the opposite side of the balance sheet - in the debts of the 99%.

And the 99% thought that, maybe, well, it [itself] could also profit financially by becoming landlords in miniature. You borrow and buy the highest price home that you can find. You could be in real estate - they thought of themselves not as wage earners, but as using their ability to earn an income, to go to the bank and pledge this income to the bank for a mortgage and buy a house that would rise in price, maybe making more money in a single year than they could earn by earning wages.

So all of that - the way in which people were spending their money and gaining wealth - was being transformed.

RADHIKA DESAI: And you know Michael, as you say, so much of the wealth in the United States over the past so many decades has become financial wealth.

And this underlines a point that our friend Jacob Assa has made in his concept of the financialization of GDP, which is that this vastly exaggerates the the wealth - because US method of counting GDP turns all this financial activity and makes it look as though it's productive activity, it vastly exaggerates the GDP of the United States, and the real wealth and income of the United States.

And of course the second thing that this reminds me of is that the inequality of the past several decades - which as most people recognize has reached astronomical levels - financialization has made a critical contribution to this and, unfortunately, although Tomas Piketty - or someone like Thomas Piketty - has documented the rise in inequality, what he has done however is he attributes it to the wrong reasons.

He makes it look as though this is the natural consequence of capitalism - and to some extent it is - but he fails to take into account the serious role - the central role - that financialization has played in inequality.

So the whole point we're trying to make is that these features of a neoliberal United States, based on financialization, have been on the one hand necessary to support the dollar system, and on the other hand they have strangulated productive activity and made the United States into a less productive and more and more unequal system.

And this policy paradigm has been continued from Reagan to Bush Senior to Clinton to Bush Junior to Obama, Trump, and today Biden.

The Democrats and the Republicans have a cross-party consensus, and this is what accounts for the parlous state of the US economy.

And in this context, it's also important to see that part of the reason why the Third World got so badly punished by the system - essentially by having to repay their debts - is that their elites, their ruling classes, did not have the courage and the political will to default.

Fidel Castro said, back in 1983-84, when the debt crisis was at its height, he said to the Latin American countries, in the eye of this storm, he said, "Don't repay your debts. These are odious debts. You don't have to repay them."

But unfortunately they did. And that's why the Third World countries suffered as much as they did.

And then what you also see in the 1980s is that the Europeans of course have - thanks to the European monetary integration and so on - they have largely absented themselves from the market for US Treasuries.

And so now the United States turns to Japan. Japan is the country that is going to that that the United States tries to inveigle into buying the enormous number of treasuries that the United States is dumping on the market in this decade because of its twin deficits - [on the one hand] the federal deficit thanks to Reaganomics, and its tax cuts and so on are increasing - and on the other hand the trade deficit is widening thanks to the deindustrialization of the United States.

So Japan in this period becomes a major buyer of US Treasuries.

michael hudson: Well [Japan] also became a general lender to other countries, and it set up more than any other country the carry trade. Because as interest rates were lowered in Japan in order to really follow the US demands - my friend David Hale, a Wall Street investment manager for Zurich International - called Japan "the thirteenth Federal Reserve District", it was creating so much money flowing over.

But it was Japanese money largely that was lent to Iceland, for the Icelandic crisis. It was lent to all sorts of other countries, because (you could borrow from) banks with low interest rates could essentially lend to other countries fueling, essentially, the whole junk bond inflation and bank crisis.

That was a byproduct that was spilling over beyond Japanese-US relations.

RADHIKA DESAI: A lot of people tried to portray, in this period, Japan as essentially somehow a victim of US policy.

But in reality, what the Japanese were doing was, first of all, they were buying US Treasuries, yes, but they were buying at a time when interest rates on these treasuries was very high. Borrowing costs were very high.

Japanese financial interests were benefiting from buying US Treasuries. And, moreover, in return, the Japanese bought "preferential access" to the US market.

In particular, as many people who are old enough to remember will remember, Japanese cars flooded American highways. This was essentially the beginning of the destruction of the American automotive industry.

The Japanese were also in the forefront of making very fuel-efficient cars which, after the two oil shocks of the 1970s, had become really very important.

This whole mechanism of essentially the United States interest rates being very high, and the Japanese buying up US Treasuries led the dollar to go to that peak that we saw in the chart earlier.

Everybody recognized that this peak was unsustainable and so the central bankers of the major financially important countries got together at the Plaza Hotel in New York to hammer out an agreement to bring the dollar lower in a controlled fashion so that it wouldn't crash and create disruptions in the market.

Again, this is often linked to the fact that this eventually led the Japanese to have a real estate bubble in Japan because the dollar went down, American interest rates went down to some extent, and therefore this created a huge inflow of money into Japan and led to massive increases in real estate prices in Japan.

And we are told that this laid the foundation for the destruction of Japan.

MICHAEL HUDSON: Well in a way it did. It did because - as you say - the Japanese were making money off this process themselves. So they themselves were a part of going along with the idea that turning from an industrial economy into a financial economy was the way to get richer.

There was so much credit that was created, that the value of the land around the palace in Tokyo - the Ginza District - was worth more than the value of all of the real estate in the United States.

Japan had essentially kept this vast increase of credit within the economy itself, as well as the carry trade, and the result was disequilibrium to say the least.

Japan did try to buy real estate in the United States. It bought a Rockefeller Center. And then it found out that it bought the land under Rockefeller Center, thinking, "Well the land value is going to go up," without realizing that the billion dollars that it spent was absolutely fixed and put it under long term at what it could charge.

So Japan said, "Okay, we see that one percent of the population is getting most of the money, so let's buy trophies, let's buy luxuries. That's what's going to go up if you're going to polarize."

So they tried to buy I think the Pebble Beach Golf Course in California, not realizing that the Pebble Beach Golf Course was not going to let them raise the money to the extent that they wanted to do it.

The Japanese investments in the United States were not very good, so they thought, somehow, that they could invest in Japan. Every month the daily Yomiuri [Shimbun] would publish - they had land prices very distinct from overall real estate prices in Japan - and you could see the steady gains, and everybody thought that buying land was going to make them rich.

Of course, all of that broke in 1990 after the Asia crisis. Ever since then, real estate prices month after month after month have gone down and down and down in Japan.

And all of this seeming financialized wealth has been dissipated.

RADHIKA DESAI: But you know what the interesting thing about Japan is Michael as you know is that the bank of Japan actually pricked the real estate bubble.

Because they knew that this is what was happening. They knew it was unsustainable. Unlike the behavior of Alan Greenspan, who always professed never to be able to see any bubble even while it was inflating under his very eyes.

So in that sense I think they pricked the bubble because while they inadvertently set off this process of financialization, Japan remains to this day a far more industrially-focused economy than the United States is.

And as a consequence their form of economic management remains quite distinct from that of the United States.

So this idea that somehow three decades of secular stagnation have destroyed Japan is actually highly exaggerated, because Japan is still a very wealthy society, and in many ways its economy is better than that of most Western countries, particularly that of the United States.

Let me just briefly quote something of mine I wrote on the subject of Japanese secular stagnation, and how it tends to be discussed in the West.

(Radhika starts reading)

The fact of the matter is, that over the past three decades of Japan's secular stagnation, there have been at least two booms that have livened an otherwise gloomy Japanese outlook. The Izanami boom of the 2000s, and the Abenomics boom of the 2010s.

As the Economist magazine noted recently, overall growth in Japan has remained sluggish, but growth per head has recently been comparable to others in G7. Unemployment has remained minimal. Longevity has increased. Inequality has stayed relatively low.

Moreover, the same Economist report quoted a 2020 tweet by Paul Krugman that pointed to another reality. Within a decade of Japan's slowdown, other major economies, including the United States, after its roaring 90s, had entered a period of low growth which appears similarly intractable.

Krugman had tweeted, "Maybe Western economists who were so critical of Japan circa 2000, myself included, should go to Tokyo and apologize to the emperor. Not that they did great, but we did much worse."

(Radhika stops reading)

So that is to say that this whole relation between financialization, productive economy, and the whole phenomenon of secular stagnation has really now come home to roost even in Western countries. So this is something we can discuss in further detail in another show.

But for now let me just say that the bond buying of Japan - the buying of US bonds - had already faded by the end of the 1980s. By the early 1990s the United States seemed to be in a real funk.

George Bush Jr lost the 1992 elections very memorably as James Carville said, because "it's the economy, stupid."

The economy was doing so badly that the incumbent president lost the elections. Remember also that this was the election - in 1992 - when Ross Perot became the most successful third party candidate I think throughout the twentieth century history of the United States. Because he ran on a platform which said, "Look at Japan. Japan is doing so well because they are not neoliberal, because they don't believe in free markets, because they have industrial policy, because they are able to be industrially powerful. That's what we need."

And he ran a really successful campaign and even managed to shift Clinton's rhetoric a little bit more in an interventionist and anti-neoliberal direction. Of course Clinton did not keep his promise because no sooner was he elected then the financial interests essentially took charge of him.

Alan Greenspan and others essentially met him and told him that if he tried to go through with his interventionist program that there would be a big run on the market against the US dollar, against US treasuries, the Federal Reserve would be forced to increase interest rates, etc.

So in any case the point is that in the 1990s, you got the whole new political economy, and this was where you begin to see the shift to the different regime of the US trying to keep the dollar as the world's money, which is by inflating asset bubbles.

And the first asset bubble to be inflated was of course Dot Com bubble. And in the prelude to that you also see Alan Greenspan, and the Treasury generally, engage in a huge drive to encourage other countries, particularly the big emerging markets of Asia, to lift capital controls.

They were told that if they lifted capital controls, all sorts of much-needed productive investment would come to that country. But in fact none of this happened. They lifted capital controls and the only type of money that flowed into the economies was short-term "hot money" which inflated various asset markets in these countries and eventually led to the East Asian financial crisis.

MICHAEL HUDSON: Well the 1990s really were the turning point in this financialization. And what happened in America was very much like what had happened in England.

You could think of Clinton as the American Tony Blair. In England there were certain things that even the Thatcherite government couldn't do to privatize. Tony Blair went much further than Thatcher in privatizing the railroads and just driving the nail into what had been Britain's industrial economy.

Well in the United States, Clinton did things that even the Reagan Administration could not have done. It took the Democratic party cloaking itself in the pretense that it was a party of labor to end financial regulations. It ended the Glass-Steagall act, which led commercial banks to become brokerage houses. That diverted credit creation away from the industrial economy into the purchase of stocks and bonds and speculative investments and real estate. And then it deregulated the commodity markets, essentially.

This was all capped by the - Clinton was really much more of an anti-labor president, explicitly, than Reagan. By (i) essentially opening up NAFTA to make sure that any tendency towards American unionization would be counted at least in the South by migrants; by (ii) cutting welfare and essentially by (iii) shifting the economy towards - letting it be run by his Treasury Secretary, Robert Rubin.

And that was sort of the Rubinomics that was turned over to the Fed under Alan Greenspan to essentially let the financial system run wild while basically ending - winding down - the American tradition of social protection of labor and consumers and the poor and welfare.

And then as you just point out, the [East] Asian crisis of 1997.

RADHIKA DESAI: The East Asian crisis was also very important in another way, which also makes, as you rightly say, the 1990s a very liminal moment, a moment of transition.

You mentioned earlier, Michael, that the IMF and the World Bank had essentially lost most of their clients in the twenty-first century, and part of this had to do with the way in which the IMF in the World Bank dealt with what were, after all, some of the most dynamic economies of the world. The economies of Korea, Malaysia, Thailand, and so on.

And the way these countries were dealt with was so harmful to them that everybody who was anybody who was involved in policy making in Third World countries were taking notes.

And they realized that the IMF and the World Bank could not be relied on at all. And the moment they had any options to them they essentially refused to take any money, they refused to go to the IMF and the World Bank.

And one of the things they did, in order to prevent ever having to go to the IMF and the World Bank, is they engaged in a process of reserve accumulation.

That is to say that, instead of having a currency crisis, they accumulated enough reserves to ensure that if there was downward pressure on their currency they could intervene in markets in order to buy their own currencies and increase the prices of their currencies. So the East Asian crisis was a big moment.

And once the East Asian crisis occurred then of course all the money that was going to these countries in order to make a quick killing returned home to the United States. And the Dot Com bubble began to go up. And of course that burst in the 2000s.

And this is also therefore another transition point because the point I was making earlier by showing the slide of interest rates was that interest rates, although they came down after the Volcker shock, remained historically high in the 1980s and 1990s. But after the Dot Com bubble burst in 2000, Alan Greenspan brought interest rates down to like one percent, and kept it there until about 2004-5 when commodity prices began to go up, putting even more downward pressure on the dollar.

So then he began to increase interest rates little bit by little bit by little bit and by the time it got to about 5.25% it had burst the new bubble that Greenspan had incubated in the US economy, which is the housing and credit bubble based on all those toxic securities that most of us now know more than we ever want to about.

So this was the bursting of the 2008 financial bubble.

MICHAEL HUDSON: Well I don't want to blame that simply on interest rates.

The bubble you're talking about was a huge financial fraud, as my colleague at the University of Missouri - Kansas City, Bill Black, has shown.

The real estate boom was largely a result of a number of crooked banks making huge loans that could not be paid - companies knew that they couldn't be repaid - to racial minorities who in the past had been blacklisted.

Until about 2000, it was very very hard for Black people to get a mortgage in this country. They were redlined, and they were restricted to particular neighborhoods. And once they would move into a neighborhood often the whole neighborhood would be torn down.

That had been a practice ever since the 1960s.

I grew up near Hyde Park, Kenwood, on the South Side near the University of Chicago. In the late 1950s, finally for the first time banks began to make loans to Black homebuyers on Dorchester Avenue where I lived. This is a block from where Obama had his house in Kenwood.

And all of a sudden, as soon as a Black family moved in, the White families began to move out, prices collapsed, speculators bought them up and sold the houses at double the price to Black people who had been waiting, finally, to move from the West Side of Chicago in to where Lake Michigan was.

So basically, all of this prejudice against the Blacks was stopped after 2000, and so the banks did begin to lend to Black people, but only at much higher interest rates, and only to buy houses that were vastly overpriced, and that could not be afforded by most families.

How do you get somebody to buy a house at double the price that it had sold just a few years ago? For one thing, you don't require a down payment. For another thing, you don't limit the mortgage loan to just twenty-five percent of what they can earn - you fake their earnings, and third, you hire corrupt property appraisers to say, "Well the house really is worth twice what it sold for two years ago."

So you had enormous bank fraud and all of this was saved by President Obama who came in as basically the lobbyist for the banking sector. He was sponsored by Robert Rubin, Clinton's treasury secretary, and by Citibank, which was singled out by the FDIC as the most incompetent and outright corrupt bank in the country.

You had basically fraud and a transformation of the character of mortgages.

RADHIKA DESAI: Absolutely, Michael. Of course we could talk for hours about the actual 2008 financial crisis and the bubble that was inflated in the first decade of this century, but we want to focus on the international aspects and the dollar system.

So let me just say very briefly however, just for the record, that I think, while you're undoubtedly right about the whole sad role of a racism in real estate politics and political economy in the United States, I do like to underline that it is actually wrong to call the 2008 crisis a subprime crisis, because that implies that most of the loans went to subprime borrowers.

In reality the banks only began lending to subprime borrowers which is the very tail end of the lending boom. Which means that the bulk of the loans that were made were to totally prime borrowers. Because otherwise it becomes very easy to say all these subprime borrowers caused the crisis. That was not it at all.

But to return to these international aspects, the fact is that the low interest rates, or what is called LIRP or ZIRP which is Low (or Zero) Interest Rate Policy - it certainly played a role in this.

While I don't doubt that banks were also quite fraudulent, the fact of the matter is that low interest rate environments create an incentive to take unreasonable risks. And in that sense - and because it still remains relevant today - the only way you can explain why [even though] the economy is tanking during covid, [yet] asset prices were going up, is because of the low interest rate policy.

But anyway the point is that the international story that is told about the 2008 financial crisis, which was told again and again and repeated again and again by the highest place people - whether it is Ben Bernanke at the Federal Reserve or Bush Jr in the White House - is that this bubble got inflated because of the so-called global savings glut, or the Asian savings glut.

And the general idea was that these Asians are saving too much. They are the ones who are essentially investing in the United States and the evidence for this was that the Chinese were buying a lot of US Treasuries and other central banks in East Asia were buying a lot of treasuries.

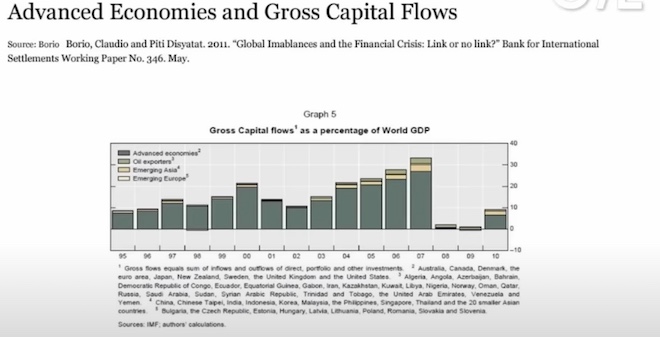

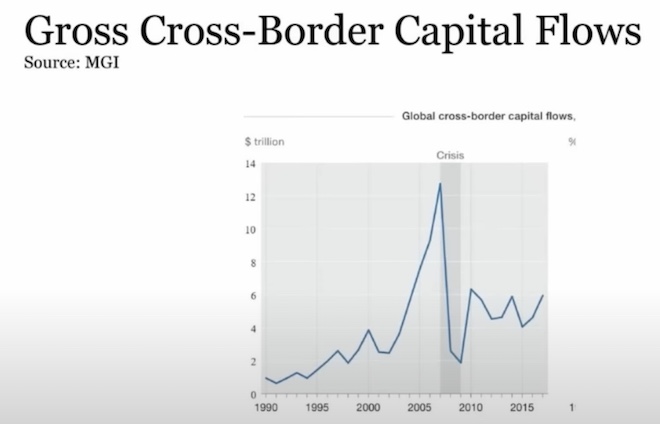

However, you see on this slide of advanced economies and gross capital flows - this is from a pay stub at the Bank of International Settlements - two economists from the Bank of International Settlements who wrote this precisely to counter this false narrative of the Asian savings glut being at the root of the 2008 financial crisis - the real cause of the financial crisis was the inflow of money primarily from Europe, from the UK and the continental Eurozone.

Because if you look at the bar, each bar shows gross capital flows around the world. And a very large proportion of these are going into the United States, and you see that the green part of each bar are the advanced economies.

And all the other parts, whether they are emerging Asia or the oil producers or whatever, represent a very small part of the total capital inflows into the United States. So what this chart tells us is that the financial crisis was a result of essentially flows from other rich countries.

And this is not surprising if you consider the fact that, while the world as a whole - you know, people call this 2008 crisis the "global" financial crisis. But you see why in this instance it's actually more accurate to call it the "North Atlantic" financial crisis.

Because the overwhelming majority of international funds that went into the toxic securities being generated by the United States were coming from Britain and from the Eurozone financial institutions, because these were the guys who gorged themselves on the toxic securities being generated.

And that is why the bulk of the financial distress was concentrated in Europe.

Of course, after the 2008 crisis, as they say, once bitten twice shy. So in this context, what happened, which you see in the next slide, is that international financial flows - you can see them peaking, reaching a huge, unprecedented peak in 2007, then falling precipitously, and then recovering, but remaining less than half of what they had been in 2007.

And this also shows us something else, which is that around this time, the idea that the United States can open a casino and invite money flowing into whatever asset bubble was going in the United States, this was beginning to fade, and increasingly the monies that are involved in US-generated asset bubbles aren't domestic US funds.

So that's really an important thing to remember, because, of course, after 2008 housing and credit bubbles have been replaced now by what we call an "everything" bubble. So every asset market is inflated, but the extent of international investment in these is considerably lower.

MICHAEL HUDSON: I don't have anything to add to that. That's right. Internationally, the Europeans have been big losers in the bubble.

For instance, the German local savings banks had bought many of the packaged mortgages that the United States was selling, and the mortgages went bad. So German savers lost a lot of money.

And the Federal Reserve bailed out these foreign banks almost just as much as they bailed out the American banks. Especially the French banks, Paribas, all of these were heavily bailed out.

But the shock - for other industrial countries investing in the US and abroad - was almost similar to the shock they had after Mexico's default in 1982.

There's a question of: Can they really collect? Is there a reality?

And they realized that so much of the financialization in the United States was not even based on interest rates but based on gambling on derivatives, on bets as to whether interest rates would go up or down, whether capital prices, stock prices, and real estate prices would go up and down.

The whole character of investment called for an entirely new generation of investment managers, and this new generation was, as we've discussed, financially-oriented, not industrially-oriented.

RADHIKA DESAI: Exactly. I should say that now we've gone for more than an hour, and we've only dealt with question one, and I still want to say one final set of things about question one. So what we're going to do is answer question two in the next show.

But for now let me bring this discussion to a conclusion by saying a couple of things.

So what we've done is, we've tried to show that what's seen as this period of easy dollar dominance after 1971, has been a heavily managed process, but also a process in which American attempts to try to manage the system in order to keep the dollar going have been full of contradictions. They have had their ups and downs.

And now we are moving into a period of serious reckoning. Because on the one hand, the Federal Reserve's capacity to generate asset bubbles and to keep money flowing into the United States is being exhausted.

Moreover, and this is the first thing I want to say, and that is that the fact that these asset bubbles now exist, and that the bulk of the wealth of rich people in the United States depends on these asset bubbles, means that the Federal Reserve is now caught in a bind.

Because on the one hand, these asset bubbles are necessary for keeping the dollar's value high, etc. But on the other hand, dealing with inflation will require increasing interest rates to an extent where this will burst these asset bubbles.

So the Federal Reserve has a choice between what's called "monetary stability" and what's called "financial stability". This is what we argued in our episode on inflation, and also which I argued in this article that I wrote entitled "Vectors of Inflation".

So basically the idea is that, if inflation goes high, the dollar's value will suffer. If the asset bubbles are burst, the dollar's value will suffer. So the Federal Reserve is caught between a rock and a hard place.

So let me just now conclude by saying the final thing I want to say about this long history of dollar boosting, which has consistently focused on denying the contradictions of the dollar system.

Because you see, throughout this period, since the 1960s the rest of the world has complained that the United States has been living beyond its means. So as early as 1961, as gold was flowing out and a gold pool had been necessary - we discussed this in the previous episode - it had been necessary to back the dollar with adequate gold, this is when you first hear the first denial that the United States was living beyond its means.

And in response to this, the United States said that, on the one hand the gold pool was going to ensure that the dollar would be backed by gold - paying no attention to the fact that the gold in the gold pool did not belong to the United States - and then going on to say, and I'm quoting from the "Economic Report of the President" - "Meanwhile the world should not doubt the dollar's international investment position.

"After all, US non-gold assets showed that the nation is not living beyond its means. Rather, its means are steadily increasing. At the end of the 1960s the US government owned foreign assets totalling twenty-one billion dollars, in addition to gold holdings of eighteen billion dollars."Of course they had been much bigger before.

To quote further,"And US citizens owned fifty billion in assets abroad. These US claims on foreigners,"the Economic Report claimed,"gave a 'basic long-run strength to the dollar' even though some of these claims were private and long-term and could not be quickly mobilized.