By David Stockman

David Stockman's Contra Corner

April 6, 2026

The Donald plunged into one hell of a hornets nest when he took the bait from Bibi Netanyahu and launched an all out "kinetic" war on Iran (as distinguished from the brutal economic war Washington has been waging for decades). But now that the gasoline pump price has breached $4/gallon and is heading higher, he's desperately looking for an off-ramp.

Yet the one he has seized upon in the last 48 hours or so is not even remotely fit for purpose. To wit, he threatens to pick up Washington's military football and go home, leaving what's left of the Iranian government-mainly the brutish IRGC-in charge of the Strait of Hormuz. That is, operating a toll booth and military checkpoint on a waterway that had been open to world commerce free of charge until the Donald foolishly unleashed bombs and missiles on Iran on February 28th.

"we don't import much oil from there anymore......within 2-3 weeks, we'll leave. That's not for us. A guy can take a mine, drop it in the water. That can be for France or whoever is using the strait".

The presumption, of course, is that because the US imports virtually no petroleum from the Persian Gulf the new Hormuz toll booth is Europe's and Asia's problem, not Washington's. And that'stechnically true but here's the spoiler alert: What matters is not the geography of where the barrels of hydrocarbon molecules are moving from and to at any given point in time, but the level of hydrocarbon prices embedded in the digital bits coursing through the global futures and cash markets all the time and everywhere.

That's because the latter reflects the markets' judgement about the state of global supply, demand and inventories in totality. Unlike the Donald, traders on the exchanges are fully familiar with the potent process of market arbitrage. In this case, it means that when the same hydrocarbon molecule has radically different prices around the planet, then some enterprising traders will buy them where the price is low and ship them to where it's high, and pocket the profit, net of shipping costs, insurance, interest carry cost and other nits and nats of market operation.

The consequence, of course, is the "law of one price" worldwide. Rather than zero exposure to the Persian Gulf's slow-steaming barrels of hydrocarbon molecules, the US has 100% exposure to Gulf-impacted digital price bits being digitally transmitted instantaneously around the planet on a 24/7 basis.

Accordingly, if the Donald thinks the oil price is going to be high in Europe and Asia because they get their hydrocarbon molecules from the Persian Gulf and low in the USA because we are 100% self-sufficient in oil and gas, he is sadly and utterly mistaken. The digital networks of the paper and cash markets will quickly equilibriate the price of hydrocarbons on a worldwide basis, and the physical barrels will not be far behind.

So lets start with the home team that the Donald thinks somehow operates as an economic island all by its lonesome, unconnected to the global markets. But for this purpose we must look at the entire oil and natural gas complex because under the law of one market petroleum and nat gas molecules are highly interchangeable. And we also measure everything in BOE (barrels of oil equivalent) in order to avoid apples and oranges on the price quotations.

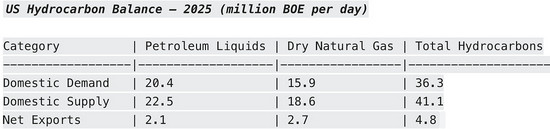

Thus, if we look at just the domestic energy patch, the massive output of the US natural gas industry--heavily driven by fracking-towers well above conventional US crude oil production, including fracked crude. To wit, in 2025 field production of natural gas (i.e. "wet gas") was 26.5 million BOE/day while crude oil and condensate from the field was 13.6 million BOE/day.

In terms of physical molecules and pricing, however, upwards of 30% of field production (7.9 million BOEs/day) of so-called "wet gas" consists of NGLs (natural gas liquids), mainly ethane, propane, butane and natural gasoline. All of these go into the same end markets-heating, cooking, petrochemicals and transportation-as similar liquids obtained from refinery runs of crude oil. The common molecules from both streams, therefore, are subject to the law of one market.

Thus, the 22.5 million BOE per day of total "petroleum liquids" supply shown in the table below includes a very large component of Natural Gas Liquids (NGLs) as follows:

- Crude oil + lease condensate: 13.6 BOE/d

- Natural Gas Liquids (NGLs): 7.9 BOE/d

- Refinery processing gain: ~1.0 BOE/d

The above hints at the price linkage between the oil and gas markets. The U.S. petrochemical industry, for instance, uses ethane as the primary feedstock for steam crackers that produce ethylene, which is the building block for plastics, packaging, and countless other products. Ethane from two main sources competes for the feedstock requirements of the steam crackers:

- Field-produced NGLs (extracted from wet natural gas at gas processing plants)

- Refinery-sourced ethane (produced as a byproduct when refineries process crude oil)

At the present time, NGL-derived ethane is generally cheaper and more abundant - especially from shale gas basins like the Permian and Marcellus owing to the continuing oversupply of natural gas. So it has captured the lion's share of U.S. cracker feedstock in recent years.

By contrast, refinery ethane tends to be more expensive and less consistent in volume, so it often serves as a secondary or swing feedstock. Moreover, when NGL supply surges or the global price of crude oil and its derivatives rise, the ethane cracker feedstock competition intensifies. On the margin, petrochemical operators shift even more heavily toward the cheaper NGL-derived ethane, thereby linking U.S. natural gas prices to the global petroleum markets.

In any event, the convention with respect to industry statistics is to include NGLs extracted from natural gas wells in the "petroleum liquids" category. So to avoid double counting, we include in the table below only the dry gas portion of nat gas field production, which gets distributed to end markets by pipelines.

Accordingly, as shown below the USA in 2025 produced 41.1 million BOE/day of combined oil and gas, which well exceeded domestic demand of 36.3 million BOE/day. The latter went into the slate of refinery products sold domestically and the pipeline delivery of nat gas to domestic end markets.

The resulting arithmetic, of course, shows that the balance of supply over demand was accounted for by 4.8 million BOE per day of exports. This was a mix of crude oil (@ 1.4 million BOE/day and refinery products (0.7 million BOE/day) under the liquids column and mainly LNG under the dry gas column.

Still, the fact that domestic supply was 113% of domestic demand, does not mean the US economy is insulated from the current massive shortfall of both gas and oil coming out of the Persian Gulf. To the contrary, it means only that the process of arbitrage between geographic markets and near-substitutes among the gas and oil streams is far more complex and subtle than the "drill, baby, drill" rhetoric that the Donald dispenses in justification of what amount to his own attack on domestic users of globally priced hydrocarbons.

Needless to say, it is the 2.1 million BOE of liquids and 2.7 million BOEs of mainly LNG under the dry gas column in the table above that provide the transmission arteries by which domestic prices are linked to global prices. In basic form, the equation is straight forward: To wit, high prices abroad and low prices domestically will cause a massive incremental draw on US exports.

That is to say, if Qatari LNG is scarce and high priced, LNG exports from the US will increase-first from fuller utilization of existing LNG plants and then over time via increased investment in liquefaction capacity. Moreover, at the present time the LNG export market draw will be especially potent if Gulf supply remains curtailed and world LNG prices stay high.

Specifically, Iran's successful attack on the huge Ras Laffan LNG facility in Qatar (and the prospect that the plant will be out of commission for up to several years) caused the Rotterdam price for LNG to soar from an average of about $69 per BOE in 2025 to current spot market quotes of @$152 per BOE.

So here is where the hidden magic of Mr. Market comes in-notwithstanding the Donald's illusion that America is an insulated island of energy plenty and cheap prices. To wit, the current spot market price for pipeline natural gas in the US at the Henry Hub terminal is about $18 per BOE. So in the language of Mr. Rogers, can you say arbitrage?

Right now the 5.8 million of BTUs in pipeline gas form at Henry Hub (Louisiana) is priced at only 12% of the landed cost of 5.8 million BTUs in LNG form at Rotterdam. In this circumstance, of course, Mr. Market would also factor in about $20 per BOE to convert US pipeline gas to liquid form at an LNG plant and another $14/BOE to ship it to Rotterdam in a specially equipped LNG tanker.

But still, the apples-to-apples cost gap would remain at about $100 per BOE-that is, $52 per BOE for US gas delivered by LNG tanker to Rotterdam versus the current spot price there of $152 per BOE.

Of course, the arbitrage doesn't work instantly and overnight. US Gulf Coast LNG plants currently have about 2.8 million BOE/day of capacity but are nearly fully utilized. So in the short run, the US/Rotterdam gap would likely just drive up spot prices and profitability on existing LNG contracts. However, there is also currently nearly 2.6 million BOE of new LNG capacity under construction in the US Gulf coast, which would nearly double current LNG export capacity when it comes on stream during the next several years.

So it is virtually guaranteed that the current $100 per BOE price gap between Rotterdam LNG and Henry Hub pipeline gas will close substantially, if shipments from the Persian Gulf remain restricted owing to Iranian military threats or just due to the delay in rebuilding the badly damaged LNG plants in Qatar and elsewhere.

More importantly, something else would happen as a second order effect that the Donald obviously hasn't reckoned with, either. The Henry Hub price for pipeline gas at $18 per BOE is low relative to WTI for light crude oil at $100 per BOE or LNG at $152 per BOE in Rotterdam owing to the nature of the pipeline gas business.

That is, domestic demand for delivered pipeline gas is pretty much driven by the level of GDP embodied in household spending and business production. So when investment in the oil patch-and especially the fracking plays--leads to excess gas supply, the spot price of pipeline gas falls. There is very little excess inventory/storage in the industry by its nature beyond the large seasonal working stocks held by the pipelines and middle men.

This is somewhat different than the case of crude oil where there is a huge long standing export market and giant waterborne tanker fleets. Prior to February 28th, there was ordinarily about 60 million BOE per day of crude oil on the blue water, carried by upwards 2,400 crude oil tankers.

So when the Brent or WTI crude oil prices rise owing to the huge supply restrictions out of the Persian Gulf the immediate impact has been the rerouting of tankers to the US crude oil terminals to take oil to Europe and Asia. In turn, that tightens the domestic supply/demand balance, pushing domestic prices higher, as well.

Accordingly, US crude and product export volumes have been and will continue to rise as long as the Gulf remains restricted and global marker prices remain high. All other things equal, in turn, this means that domestic petroleum prices will rise and stay high, as well.

In the case of natural gas, the response time and arbitrage pathways move a little more slowly, but the market dynamic is the same: As more excess US pipeline gas is drawn into the rapidly expanding US LNG plants and thereby into the global export markets, the Henry Hub pipeline gas price will rise as the current surplus of gas "deliverability" is reduced. In turn, the gas bills of homeowners and business users will go up.

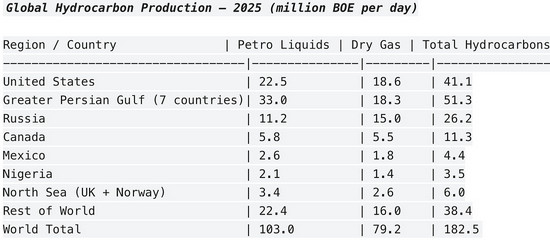

In short, the global hydrocarbon market is highly integrated and with the rise of the LNG sector and growing LNG tanker fleet has become more seamless than ever under the one price rule of markets. In this context, the US production in 2025 of 41.1 million BOEs per day of petro liquids and nat gas was nearly as large as the 51.3 million BOEs per day coming out of the Persian Gulf. ((Saudi Arabia, Iraq, UAE, Iran, Kuwait, Qatar, and Oman).

By way of comparison, total Russian hydrocarbon production was 26.2 million BOEs or just 64% of the US output and Canada at 11.3 million BOE per day was barely 25% of the US total.

In short, when you look at the entire global oil and nat gas market at 182.5 million BOEs per day it is obvious that there are two giant hydrocarbon supply nodes-the USA and the Persian Gulf. There is no way on god's green earth, however, that these giant hydrocarbon supply nodes could co-exist in splendid isolation.

Thus, having radically destabilized the world's breadbasket of hydrocarbons and all their derivatives- LPGs, fertilizer, helium, sulfur and more--that Donald's assurance that America can remain a low price oasis in a $100 +per barrel world is a barking delusion.

To the contrary, as the sign in the store used to say, if you break it, you own it. The Donald did-so now he does.

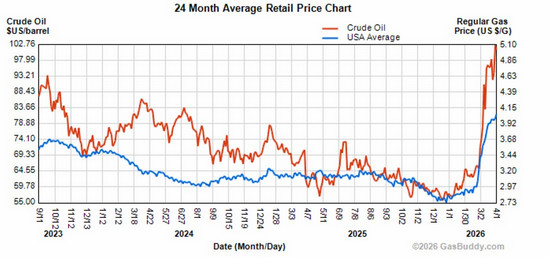

For want of doubt, here is the path of the global marker crude oil during the past 24 months versus the national average pump price of gasoline in the US. The correlation is tighter than a drum owing to the arbitrage mechanisms outlined above.

In any event, global crude oil was at $60 per barrel at the beginning of 2026 and the national average pump price stood at $2.75 per gallon, eliciting a noisy chorus of atta boys from MAGA-land.

No more. It's a global market where pricing pressures transmit rapidly accross markets and among various related elements of the hydrocarbon supply system. With global crude oil above $100 per barrel the domestic gas pump price is now at $4.03 per gallon for one reason and one reason only: The Donald kissed Bibi Netanyahu's ass and joined his war of aggression not only against Iran but the entire Persian Gulf supply system for no good reason of America's Homeland Security whatsoever.

Reprinted with permission from David Stockman's Contra Corner.